Savings vs Debt Payoff: Which Should Come First?

Should you save money or pay off debt first? Get a math-based answer.

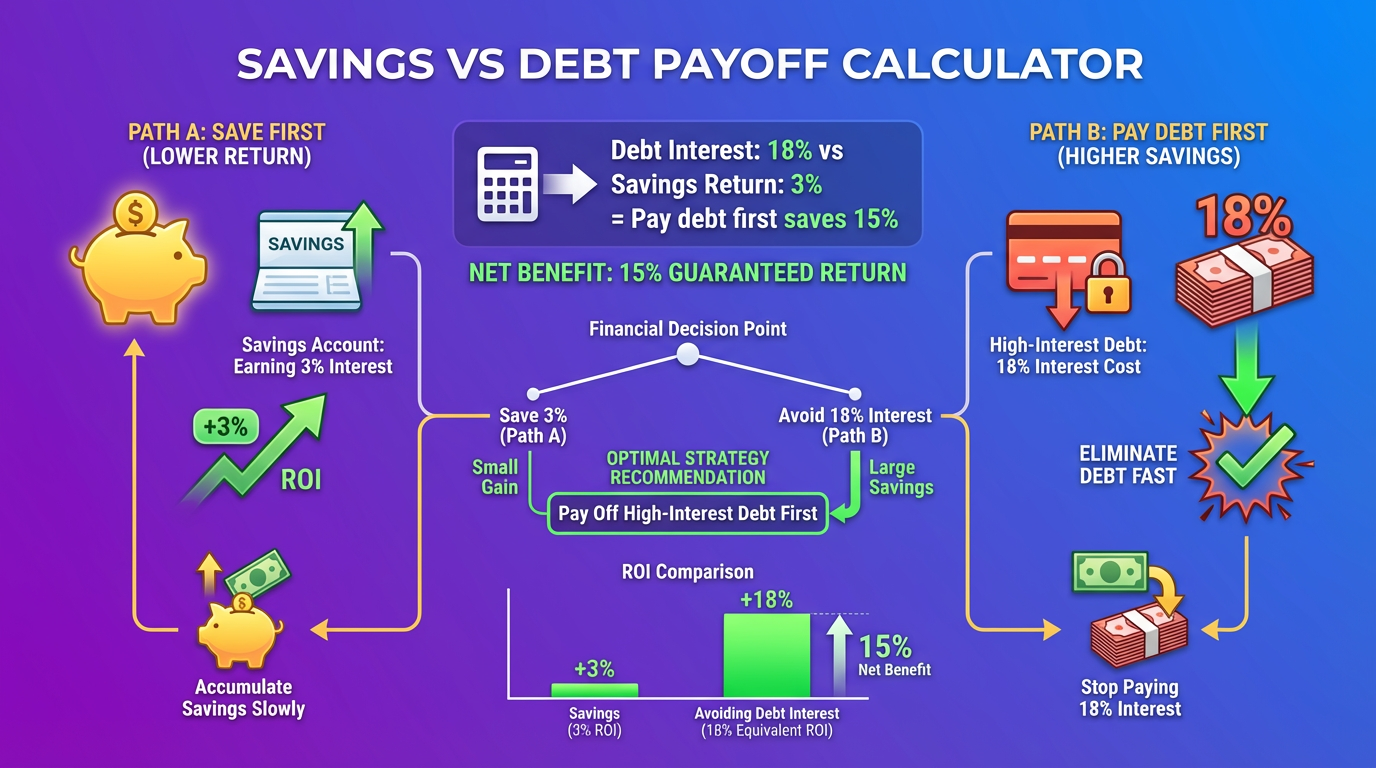

How This Savings vs Debt Payoff Calculator Works

Our savings vs debt payoff calculator helps you decide where extra money should go. Compare:

- Net worth with each strategy – Which builds more wealth✓

- Interest paid vs earned – The math behind the decision

- Emergency fund impact – Risk of having no savings

- Debt freedom timeline – When you’ll be debt-free

- Optimal hybrid approach – Balance both goals

Stop guessing. See the math for your specific situation.

The Great Debate: Save or Pay Debt✓

The Core Question

When you have extra money, you face a choice: 1. Build savings – Earn interest, create security 2. Pay off debt – Eliminate interest, reduce obligations

The mathematical answer: Compare interest rates – If debt rate > savings rate → Pay debt first – If savings rate > debt rate → Save first

But real life is more complex.

Why This Isn’t Just Math

Factors beyond interest rates:

| Factor | Favors Saving | Favors Debt Payoff |

|---|---|---|

| Job security | Uncertain job | Stable employment |

| Emergency fund | None or small | 3-6 months saved |

| Interest rate gap | Small (<5%) | Large (>10%) |

| Debt stress | Low | High |

| Tax benefits | 401(k) match available | No match available |

| Risk tolerance | Risk-averse | Comfortable with risk |

Savings vs Debt Examples: The Math

Example 1: High-Interest Credit Card Debt

Scenario: Alex has $8,000 in credit card debt and $500/month extra.

The Numbers: – Credit card APR: 22% – Savings account APY: 4.5% – Extra monthly cash: $500

Option A: Pay Debt First – Focus $500 on debt – Debt-free in: 18 months – Interest paid: $1,466 – Then save $500/month for 6 months – 2-year end position: $3,000 savings, $0 debt

Option B: Save First – Save $500/month for 6 months = $3,000 – Interest earned: ~$68 – While debt grows with minimum payments – Debt after 6 months: $7,200 (minimums only) – Then pay debt…

Comparison at 24 Months:

| Strategy | Savings | Debt | Net Worth |

|---|---|---|---|

| Pay Debt First | $3,090 | $0 | +$3,090 |

| Save First | $3,135 | $2,100 | +$1,035 |

Winner: Pay Debt First – By $2,055 in net worth.

Why: 22% debt interest far exceeds 4.5% savings interest.

Example 2: Low-Interest Auto Loan

Scenario: Maria has $12,000 auto loan and $400/month extra.

The Numbers: – Auto loan APR: 4.5% – Investment return: 8% (index funds) – Extra monthly cash: $400

Option A: Pay Off Car Faster – Add $400 to $350 car payment = $750/month – Car paid off in: 17 months (vs 36 months) – Interest saved: $850 – Then invest $750/month for 19 months – 3-year end position: $15,600 invested, $0 debt

Option B: Invest the Extra – Invest $400/month for 36 months – Continue $350 car payment for 36 months – 3-year end position: $15,850 invested, $0 debt

Comparison at 36 Months:

| Strategy | Investments | Debt | Net Worth |

|---|---|---|---|

| Pay Off Car | $15,600 | $0 | +$15,600 |

| Invest Extra | $15,850 | $0 | +$15,850 |

Winner: Invest Extra – By $250 in net worth.

Why: 8% investment return exceeds 4.5% loan rate. The spread is small, so it’s close.

Consideration: Investing involves risk; the car payoff is guaranteed return.

Example 3: Student Loans vs. Emergency Fund

Scenario: David has $35,000 in student loans, no emergency fund, $600/month extra.

The Numbers: – Student loan APR: 6.8% – Savings account APY: 4.5% – Extra monthly cash: $600 – Monthly expenses: $3,500

Option A: Attack Debt (No Emergency Fund) – Put all $600 toward loans – Pay off in: 5.5 years – Interest paid: $7,100 – Risk: Job loss = disaster

Option B: Build Emergency Fund First – Save $600/month for 6 months = $3,600 (1 month expenses) – Then $600/month toward debt for 5 years – Pay off in: 5.5 years – Interest paid: $7,400 – Risk: Protected against 1-month emergency

Option C: Balanced Approach (Recommended) – $200/month to savings, $400 to debt – After 6 months: $1,200 saved, $2,400 debt paid – After 12 months: $2,400 saved (building), debt reducing – Continue until 3-month emergency fund ($10,500) – Then redirect all $600 to debt

5-Year Comparison:

| Strategy | Savings | Debt Remaining | Net Worth | Risk Level |

|---|---|---|---|---|

| All to Debt | $0 | $8,000 | -$8,000 | HIGH |

| E-Fund First | $3,600 | $8,500 | -$4,900 | Medium |

| Balanced | $10,500 | $12,000 | -$1,500 | LOW |

Best Choice: Balanced approach – slightly less net worth, much lower risk.

Example 4: Mortgage vs. Retirement

Scenario: The Johnsons have a mortgage and 401(k) option with match.

The Numbers: – Mortgage balance: $280,000 – Mortgage rate: 6.5% – 401(k) match: 100% up to 6% of salary – Combined salary: $120,000 – Extra monthly: $1,000

Option A: Extra Mortgage Payments – Put $1,000/month extra toward mortgage – Save 13 years on mortgage – Interest saved: $156,000 – Miss $7,200/year in matching funds

Option B: Maximize 401(k) Match – Contribute 6% ($600/month) to get match – Employer adds $600/month – $400/month to mortgage – Receive $7,200/year in “free money”

25-Year Comparison:

| Strategy | 401(k) Value | Mortgage Savings | Total Benefit |

|---|---|---|---|

| All to Mortgage | $0 match | $156,000 | $156,000 |

| Get the Match | $612,000* | $85,000 | $697,000 |

*Assumes 8% return on $1,200/month for 25 years

Winner: Get the Match First – By $541,000.

The match is 100% return – no mortgage payment beats that.

Example 5: Multiple Debts, Small Savings

Scenario: Lisa has multiple debts and only $1,200 savings.

Current Situation: – Emergency fund: $1,200 (less than 1 month) – Credit card: $6,500 at 24% – Car loan: $8,000 at 6% – Extra monthly: $500

The Question: Build emergency fund or attack credit card✓

Analysis:

| Approach | Risk | Math |

|---|---|---|

| $500 to e-fund | Credit card grows | Interest: $130/month |

| $500 to credit card | No emergency buffer | Pay off in 15 months |

| $250 each | Moderate both | E-fund grows slower, debt shrinks |

Optimal Strategy: 1. Month 1-4: $300 to savings, $200 to credit card (reach $2,400 e-fund) 2. Month 5+: $500 to credit card (attack high interest) 3. After credit card paid: $500 to car, then max savings

Result at 24 Months: – Emergency fund: $2,400 (maintained) – Credit card: Paid off – Car loan: Reduced significantly – Protected AND progressing

The Priority Framework

The Proven Order

Financial experts generally recommend this sequence:

- Minimum payments on all debts – Avoid penalties

- Starter emergency fund – $1,000-$2,000

- 401(k) match – Free money (100% return)

- High-interest debt – Anything above 7-8%

- Full emergency fund – 3-6 months expenses

- Medium-interest debt – 4-7%

- Retirement savings – Max 401(k)/IRA

- Low-interest debt – Below 4%

- Additional investing – Taxable accounts

The Math Behind the Order

| Priority | Why This Order |

|---|---|

| 1. Minimums | Late fees/penalties exceed any savings benefit |

| 2. Starter e-fund | Prevents new debt from emergencies |

| 3. 401(k) match | 100% return beats all debt interest |

| 4. High-interest debt | 15-25% guaranteed return |

| 5. Full e-fund | Job loss protection |

| 6. Medium debt | 5-7% guaranteed return |

| 7. Retirement | Tax advantages, compound growth |

| 8. Low debt | 3-4% may be worth carrying |

| 9. Taxable investing | After tax-advantaged full |

When to Break the Rules

Save First (Even With High-Interest Debt)

✓ Save first if: – Job is unstable or layoffs announced – No emergency fund whatsoever – Medical issues requiring reserves – Freelance/variable income – Major known expense coming (baby, etc.) – Mental health requires security feeling

How much: At minimum, 1 month of expenses before attacking debt.

Pay Debt First (Even Before Saving)

✓ Pay debt first if: – Stable job with good security – Already have 1+ month expenses saved – Debt interest exceeds 15%+ – Debt is growing faster than you can save – Spouse has emergency savings access – Low expenses / could reduce quickly if needed

Interest Rate Breakeven Analysis

When Does Saving Beat Paying Debt✓

The formula:

If: Investment Return > Debt Interest Rate

Then: Investing may win

But factor in:

- Investment risk (not guaranteed)

- Tax impact (retirement accounts)

- Emotional cost of debtRealistic comparisons:

| Debt Rate | Savings Rate | Winner |

|---|---|---|

| 25% (credit card) | 5% savings | Pay debt |

| 20% (credit card) | 8% investing | Pay debt |

| 15% (store card) | 8% investing | Pay debt |

| 8% (personal loan) | 8% investing | Toss-up |

| 6% (auto loan) | 8% investing | Slight save edge |

| 4% (student loan) | 8% investing | Save/invest |

| 3% (mortgage) | 8% investing | Save/invest |

Key insight: Stock market averages 8-10%, but isn’t guaranteed. Debt payoff is guaranteed return.

Frequently Asked Questions

Should I save or pay off debt first✓

Quick decision guide:

| Your Situation | Recommendation |

|---|---|

| No emergency fund | Save $1,000-$2,000 first |

| Credit card debt (15%+) | Pay debt (after e-fund) |

| 401(k) match available | Get full match first |

| Low-interest debt (<6%) | Can invest simultaneously |

| Unstable job | Prioritize savings |

For most people: Small emergency fund → 401(k) match → high-interest debt → full emergency fund → everything else.

How much emergency fund do I need before paying debt✓

Recommended amounts:

| Employment Type | Minimum E-Fund |

|---|---|

| Very stable job | 1-2 months expenses |

| Average stability | 3 months expenses |

| Unstable/seasonal | 6 months expenses |

| Self-employed | 6-12 months expenses |

While paying high-interest debt: 1-2 months minimum, build to 3-6 after debt paid.

Is it better to save or pay off credit cards✓

Almost always pay credit cards first (after minimal emergency fund).

Why: – Credit card rates: 18-28% – Savings rates: 4-5% – The gap: 15-23% in debt’s favor

Exception: If you’ll lose your job next month, having cash matters more.

Should I stop 401(k) to pay off debt✓

Don’t stop contributions if you have employer match.

| Scenario | Recommendation |

|---|---|

| Employer matches | Contribute up to match |

| No match, 20%+ debt | May pause 401(k) temporarily |

| No match, <10% debt | Continue contributing |

The match is free money – even 20% credit card debt doesn’t beat 100% return.

What about high-yield savings vs paying debt✓

Current high-yield rates: 4-5% Credit card rates: 18-25%

Math: Paying credit card debt = 18-25% guaranteed return High-yield savings = 4-5% return

Pay the debt. Even if HYSA offered 10%, credit card payoff wins.

Does debt payoff or saving build more wealth✓

Long-term wealth formula:

Pay off high-interest debt fast →

Free up payments →

Invest freed payments →

Compound growth →

Maximum wealthCarrying 20% debt while saving 5% destroys wealth. Getting debt-free faster accelerates wealth building.

What if I have low-interest debt✓

Low interest (under 6%) is different:

| Scenario | Consider |

|---|---|

| Mortgage at 3% | May be better to invest |

| Auto at 4.5% | Borderline – your preference |

| Student at 5% | Invest if rate higher, or focus on debt for simplicity |

Psychological factor: Some people prefer debt-free over maximum returns. Both are valid.

Should I drain savings to pay off debt✓

Generally no. Keep at least: – $1,000 absolute minimum – Ideally 1 month expenses

Why: Emergency without savings = new debt (often worse terms).

Exception: If you have credit available for true emergency AND debt is very high interest, strategic drain can work.

How do I balance multiple goals✓

Use percentages of extra money:

| Situation | Savings | Debt | Investing |

|---|---|---|---|

| No e-fund, high debt | 60% | 40% | 0% |

| Small e-fund, high debt | 20% | 80% | 0% |

| E-fund OK, high debt | 0% | 100% | 0% |

| E-fund OK, low debt | 0% | 50% | 50% |

| No debt | 20% | 0% | 80% |

Adjust percentages based on your risk tolerance and debt rates.

What’s the psychological benefit of paying off debt✓

Studies show debt causes: – Stress and anxiety – Sleep problems – Relationship strain – Decision fatigue

Many people report: – Immediate relief when debt paid – Motivation from progress – Freedom feeling

The “best” mathematical answer may not be the best for YOU if debt causes significant stress.

Is paying off mortgage or investing better✓

The classic debate:

| Factor | Pay Mortgage | Invest |

|---|---|---|

| Return | 6-7% (guaranteed) | 8-10% (historical, not guaranteed) |

| Risk | Zero | Market fluctuations |

| Liquidity | Low (home equity) | High (sell investments) |

| Tax impact | Deduction decreases over time | Tax-advantaged growth |

| Emotional | Peace of ownership | May feel like “more progress” |

Common approach: Get 401(k) match, then split extra between mortgage and investing.

What if interest rates change✓

Review your strategy when: – Savings rates change significantly (±1%) – You can refinance debt to lower rate – Investment returns shift dramatically – Your income or stability changes

The 8% rule: If debt rate is above 8%, pay it. Below 8%, consider investing. Near 8%, personal preference matters.

Related Calculators

Optimize your financial strategy:

- Emergency Fund Calculator – How much do you need✓

- Debt Snowball vs Avalanche – Best payoff method

- Compound Interest Loss Calculator – Cost of delayed investing

- Credit Card Payoff Calculator – Plan your payoff

This calculator provides estimates based on rates you enter. Investment returns aren’t guaranteed. Consider consulting a financial advisor for personalized guidance.