Debt Stress Cost Calculator: The Hidden Price You're Paying

Calculate the hidden costs of debt-related stress on your health, work, and finances.

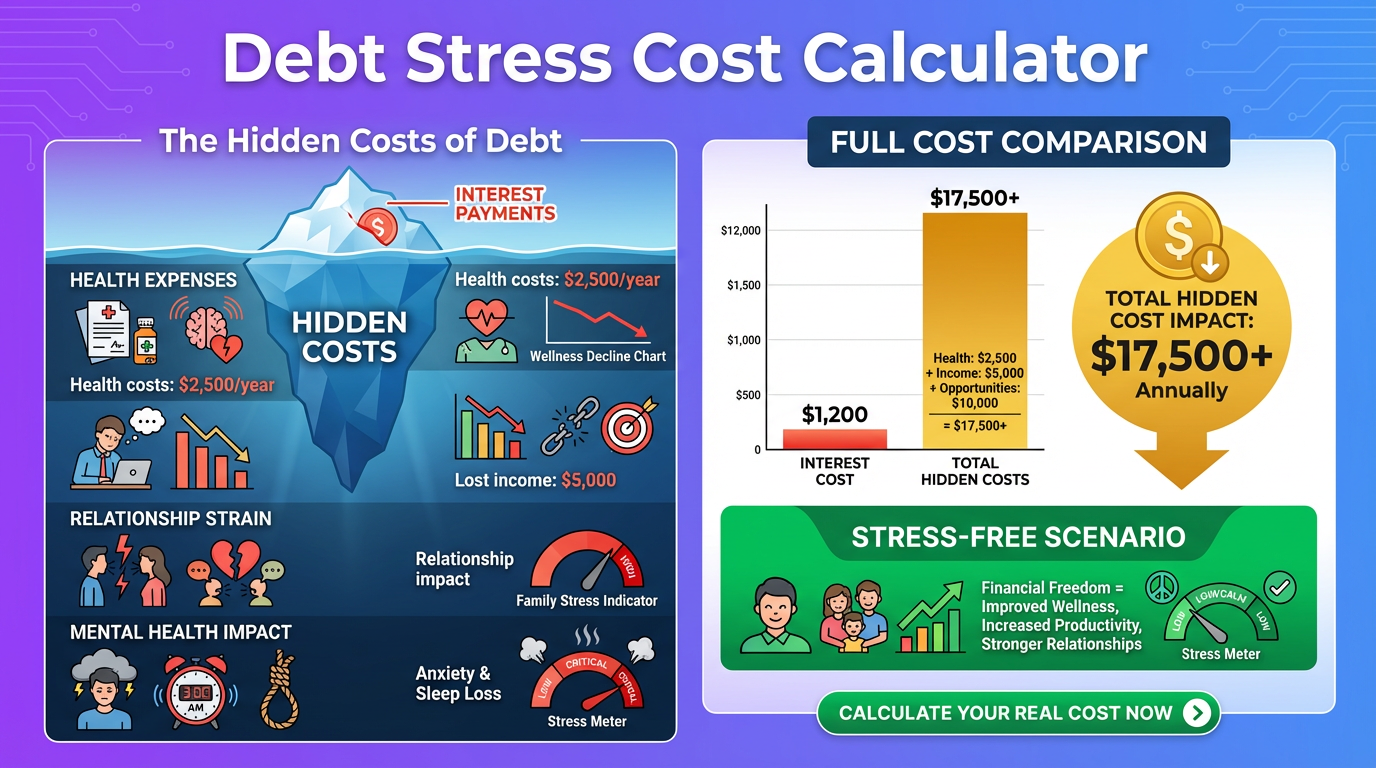

How This Debt Stress Cost Calculator Works

Our debt stress cost calculator reveals the hidden price of financial worry that doesn’t show up on your statements. See:

- Health-related costs – Medical expenses linked to stress

- Productivity losses – Work impact from financial distraction

- Relationship costs – Strain on partnerships and family

- Lost opportunities – What you miss while stressed about debt

- Quality of life impact – The intangible toll

Debt costs more than interest. It costs your health, relationships, and happiness.

The Science of Debt Stress

What Research Tells Us

Financial stress is the #1 source of stress for Americans (American Psychological Association).

Key findings: – 72% of Americans feel stressed about money at least sometimes – 22% experience extreme financial stress – Debt-related stress increases risk of depression by 3x – High debt is linked to higher blood pressure and worse immune function

The Stress-Debt Cycle

Debt → Stress → Poor decisions → More debt → More stressBreaking the cycle requires addressing both the debt AND the stress.

Debt Stress Cost Examples: Real Impact

Example 1: Health Costs of Credit Card Stress

Scenario: Marcus carries $18,000 in credit card debt and experiences significant stress.

Health Impacts Over 3 Years:

| Health Issue | Frequency | Cost Per Occurrence | 3-Year Total |

|---|---|---|---|

| Doctor visits (stress symptoms) | 4/year | $150 copay | $1,800 |

| Prescription medications | Ongoing | $45/month | $1,620 |

| ER visit (chest pain/anxiety) | 2 total | $500 copay | $1,000 |

| Therapy sessions | 12/year | $50 copay | $1,800 |

| Sick days taken | 6/year | $200/day lost | $3,600 |

| Total Health Costs | — | — | $9,820 |

Comparison to Debt Interest: – Interest paid on $18K debt over 3 years: ~$8,500 – Health costs from stress: $9,820 – Stress costs MORE than the interest

Hidden multiplier: Stress may delay career advancement (raises, promotions), adding thousands more in lost income.

Example 2: Productivity and Career Impact

Scenario: Jennifer has $45,000 in combined debt and spends significant mental energy worrying.

Workplace Productivity Analysis:

| Impact Area | Estimate | Calculation | Annual Cost |

|---|---|---|---|

| Time distracted at work | 30 min/day | 125 hrs/year | 3% of work time |

| Projects delayed | 2/year | Slower advancement | Hard to quantify |

| Missed networking | Monthly events | Relationship building | Hard to quantify |

| Declined promotion | 1 in 3 years | $8,000 raise missed | $8,000/year ongoing |

Salary Impact: – Current salary: $65,000 – Missed promotion: $73,000 (would have been) – Annual loss: $8,000 – Over 10 years: $80,000+ (with compounding raises)

Research shows: Workers with financial stress are: – 5x more likely to be distracted at work – 2x more likely to miss work – Less likely to take risks (like asking for promotions)

Example 3: Relationship Strain

Scenario: The Andersons have $55,000 in debt and argue about money regularly.

Relationship Costs:

| Impact | Description | Estimated Cost |

|---|---|---|

| Couples therapy | 20 sessions at $150 | $3,000 |

| Separate purchases (hiding) | Undisclosed spending | $2,000/year |

| Foregone family activities | Vacations, outings skipped | $3,500/year |

| Divorce attorney (if it goes there) | Initial consultation | $500 |

| Potential divorce costs | Average divorce: $15,000-$30,000 | — |

Statistics: – Money is the #1 topic couples argue about – Couples with debt are 2x more likely to divorce – Financial stress reduces relationship satisfaction by 30%

The Andersons’ 3-Year Relationship Costs: – Therapy: $3,000 – Hidden spending discovered: $4,000 – Missed family experiences: $10,500 – Total: $17,500 (not including potential divorce)

Example 4: Opportunity Costs of Stress

Scenario: David has $30,000 in debt and is too stressed to pursue opportunities.

Opportunities Declined or Missed:

| Opportunity | Reason Declined | Potential Value |

|---|---|---|

| Job in new city | Couldn’t afford moving costs | $15,000 salary increase |

| Side business idea | No mental bandwidth | Unknown (possibly significant) |

| Investment opportunity | Needed all cash for debt | $5,000 return over 3 years |

| Professional certification | Couldn’t focus to study | $7,000 salary bump |

| Vacation (stress relief) | Couldn’t justify expense | Immeasurable health benefit |

5-Year Opportunity Cost: – Declined job: $75,000 (salary difference × 5 years) – Certification not pursued: $35,000 (salary bump × 5 years) – Investment missed: $5,000 – Total: $115,000 in foregone opportunities

The paradox: Stress about $30,000 in debt led to $115,000 in missed opportunities.

Example 5: Sleep and Health Cascade

Scenario: Lisa’s $22,000 debt causes chronic sleep problems.

The Sleep-Debt Connection:

| Stage | Impact | Consequence |

|---|---|---|

| Worry at bedtime | 1-2 hours less sleep/night | Sleep deprivation |

| Sleep deprivation | Reduced cognitive function | Worse decisions |

| Fatigue | Lower productivity | Career stagnation |

| Weakened immunity | More illness | Health costs |

| Weight gain | Stress eating, cortisol | Long-term health issues |

Annual Costs of Sleep Disruption:

| Cost Category | Amount |

|---|---|

| OTC sleep aids | $300 |

| Extra coffee/energy drinks | $500 |

| Sick days (reduced immunity) | $1,200 |

| Impulse purchases (tired brain) | $1,800 |

| Fast food (too tired to cook) | $2,400 |

| Total | $6,200 |

10-Year Projection: – Direct sleep-related costs: $62,000 – Long-term health impact: Potentially much higher – Quality of life: Significantly diminished

The Full Cost of Debt Stress

Cost Categories

| Category | Examples | Typical Annual Cost |

|---|---|---|

| Direct Health | Doctor visits, medications, ER | $1,500-$5,000 |

| Mental Health | Therapy, counseling, medications | $1,200-$6,000 |

| Lost Productivity | Work distraction, sick days | $2,000-$10,000 |

| Career Impact | Missed promotions, raises | $5,000-$20,000 |

| Relationship | Therapy, separate spending, divorce | $2,000-$30,000 |

| Opportunity Cost | Declined opportunities | $5,000-$50,000 |

| Quality of Life | Foregone experiences | Priceless |

Total Hidden Cost Estimate

For someone with $25,000 in high-interest debt:

| Cost Type | Conservative | Moderate | High |

|---|---|---|---|

| Interest paid | $5,000/yr | $5,000/yr | $5,000/yr |

| Hidden stress costs | $3,000/yr | $8,000/yr | $20,000/yr |

| True annual cost | $8,000 | $13,000 | $25,000 |

The hidden costs can exceed the interest payments.

Stress Symptoms Linked to Debt

Physical Symptoms

| Symptom | Prevalence in Debt Stress | Notes |

|---|---|---|

| Headaches | 44% | Tension-type common |

| Muscle tension | 39% | Neck, shoulders, back |

| Fatigue | 51% | Chronic tiredness |

| Sleep problems | 56% | Insomnia, poor quality |

| Digestive issues | 34% | IBS, upset stomach |

| Elevated blood pressure | 27% | Cardiovascular risk |

| Weakened immunity | 23% | More frequent illness |

Mental/Emotional Symptoms

| Symptom | Prevalence in Debt Stress | Notes |

|---|---|---|

| Anxiety | 65% | Constant worry |

| Depression | 42% | Hopelessness, low mood |

| Irritability | 48% | Short temper |

| Difficulty concentrating | 53% | Mental fog |

| Loss of motivation | 38% | Paralysis, avoidance |

| Shame/embarrassment | 67% | Social withdrawal |

| Hopelessness | 29% | Feeling trapped |

Behavioral Changes

| Behavior | Prevalence | Cost Impact |

|---|---|---|

| Avoiding bills/statements | 34% | Late fees, worse problems |

| Retail therapy | 28% | More debt |

| Substance use increase | 15% | Health, additional costs |

| Social withdrawal | 31% | Lost relationships |

| Arguing with partner | 56% | Relationship damage |

| Neglecting health | 27% | Future medical costs |

Breaking the Stress-Debt Cycle

Step 1: Acknowledge the True Cost

Calculate YOUR stress costs: – Health expenses related to stress – Sick days and productivity loss – Relationship strain – Opportunities declined

Seeing the full picture motivates action.

Step 2: Address Both Debt AND Stress

For the debt: – Use our Debt Snowball Calculator – Consider Debt Consolidation – Make a written plan (reduces anxiety)

For the stress: – Exercise (proven stress reducer) – Sleep hygiene improvements – Professional support if needed – Financial education (knowledge reduces fear)

Step 3: Celebrate Progress

Each payment: – Reduces debt – Reduces interest – Reduces stress – Improves health

Track non-financial wins: – Sleeping better – Fewer arguments – More energy – Better focus

Step 4: Prevent Recurrence

Once debt-free: – Build emergency fund – Create spending plan – Develop savings habits – Maintain financial education

Frequently Asked Questions

How does debt affect mental health✓

Research shows debt is linked to: – 3x higher risk of depression – Higher rates of anxiety disorders – Increased suicide risk (severe cases) – Lower overall life satisfaction

Mechanisms: – Constant worry consumes mental resources – Shame leads to social isolation – Hopelessness develops over time – Sleep disruption affects brain chemistry

Professional help is available and effective—don’t hesitate to seek it.

What are physical symptoms of financial stress✓

Common physical manifestations: – Headaches and migraines – Muscle tension (neck, shoulders, back) – Digestive problems (stomach upset, IBS) – Sleep disturbances – Fatigue and low energy – Elevated blood pressure – Weakened immune system – Weight changes

These are real medical symptoms that often improve when financial stress is addressed.

How much does debt stress cost in health expenses✓

Estimates vary, but research suggests: – $1,500-$5,000/year in additional health costs – 50% more doctor visits than non-stressed peers – Higher rates of expensive ER visits – Increased medication needs

One study found: People with debt stress have 76% higher healthcare costs than those without.

Does paying off debt reduce stress✓

Yes—and quickly.

Studies show: – Stress reduction begins with first payment – Each milestone (25%, 50%, 75% paid) brings relief – Becoming debt-free improves happiness scores by 30-40% – Effects are immediate and lasting

Creating a plan alone reduces stress even before payments begin.

How does debt affect relationships✓

Money is the #1 topic couples argue about.

Debt specifically causes: – Blame and resentment – Hiding spending (financial infidelity) – Reduced intimacy – Canceled shared activities – Higher divorce rates (2x for couples with debt)

Addressing debt together can actually strengthen relationships.

Can financial stress cause insomnia✓

Absolutely. Financial worry is a leading cause of sleep problems.

The cycle: 1. Worry about bills at bedtime 2. Poor sleep quality 3. Fatigue and poor decisions next day 4. Financial mistakes worsen 5. More worry at bedtime

Breaking it: Create a “worry time” earlier in day, write down a plan before bed, practice relaxation techniques.

What’s the productivity cost of debt stress✓

Research estimates: – 15-20 hours/month lost to financial distraction – 5x more likely to miss work – 40% reduction in workplace performance – Career advancement delays

For $60,000 salary: 20% productivity loss = $12,000/year in value lost to employer (and potentially you in missed advancement).

Should I get therapy for debt stress✓

Consider professional help if: – Stress interferes with daily life – You’re experiencing depression or anxiety symptoms – You’re avoiding dealing with finances completely – Relationships are suffering significantly – You’re having physical health symptoms

Therapy can: – Provide coping strategies – Address underlying issues – Help create action plans – Improve overall functioning

Many therapists offer sliding scale fees; some employers provide EAP benefits.

How do I stop worrying about debt✓

Worry management strategies:

- Create a written plan – Uncertainty causes anxiety; plans reduce it

- Set “worry time” – 15 minutes/day to address concerns, then move on

- Automate payments – Remove daily decision-making

- Track progress – Seeing improvement motivates

- Focus on what you control – Payment amount, not interest rates already set

- Practice gratitude – Balance worry with appreciation

- Limit financial media – Reduce triggers

- Exercise regularly – Proven anxiety reducer

Does debt stress affect children✓

Yes, children absorb parental financial stress:

Impact on children: – Anxiety and worry behaviors – Academic performance decline – Behavioral problems – Relationship with money (positive or negative) – Long-term financial habits

Protecting children: – Don’t argue about money in front of them – Be honest in age-appropriate ways – Model healthy coping – Teach positive financial habits – Reassure about basic security

Can stress lead to more debt✓

Yes—this is the stress-debt cycle:

- Emotional spending – “Retail therapy” for stress relief

- Poor decisions – Tired, stressed brains make mistakes

- Avoidance – Not opening bills makes problems worse

- Health costs – Stress-related medical expenses

- Lost income – Productivity decline, missed opportunities

Breaking the cycle requires addressing both the debt and the stress simultaneously.

What’s the ROI of reducing debt stress✓

Potential returns:

| Investment | Potential Return |

|---|---|

| Debt payoff plan (free) | Reduced anxiety immediately |

| Financial counseling ($200) | Better strategy, less waste |

| Therapy (1, 500/year)|Improvedfunction,relationships||Debtpayoff(X) | All stress costs eliminated |

Compare to stress costs: If stress costs $8,000/year and debt payoff costs $8,000, payoff has infinite ROI by eliminating ongoing stress expense.

Related Calculators

Take control of your financial stress:

- Debt Snowball vs Avalanche Calculator – Create your payoff plan

- Financial Freedom Date Calculator – See your debt-free date

- Credit Card Payoff Calculator – Plan credit card elimination

- Emergency Fund Calculator – Build your safety net

This calculator provides estimates of stress-related costs based on research averages. Individual experiences vary. If you’re experiencing significant stress, anxiety, or depression, please consult a healthcare professional.