You’re $15,000 deep in credit card debt, paying $500 a month that barely makes a dent in your balances. A friend mentions debt consolidation, and you wonder: “If I’m already drowning in debt, how does taking on MORE debt help? Isn’t that just digging the hole deeper?”

It’s a logical question. On the surface, borrowing money to pay off money you borrowed seems circular, like using one credit card to pay off another.

But thousands of LendWyse customers who asked this exact question discovered something surprising: the right kind of debt consolidation doesn’t just move your problem around. It fundamentally changes the math of your debt in ways that accelerate freedom rather than prolonging bondage.

Let’s explore real outcomes from actual people who were skeptical about whether consolidation was worth it when they were already buried in debt.

Table Of Contents:

- The Paradox: More Debt That Reduces Debt

- Real Outcome #1: From Endless Treadmill to a Clear Finish Line

- Real Outcome #2: Immediate Psychological Relief

- Real Outcome #3: Dramatic Interest Savings

- Real Outcome #4: Simplified Financial Life

- Real Outcome #5: Credit Score Improvement

- Real Outcome #6: Breaking the Reaccumulation Cycle

- Real Outcome #7: Regaining Financial Control

- When Consolidation ISN’T Worth It

- The Alternatives When Consolidation Isn’t the Answer

- The Total Value Calculation

- The Decisive Question

- The Timing Question: Is Now the Right Time?

- The Bottom Line: Is It Worth It?

- Ready to Discover Your Real Outcomes?

The Paradox: More Debt That Reduces Debt

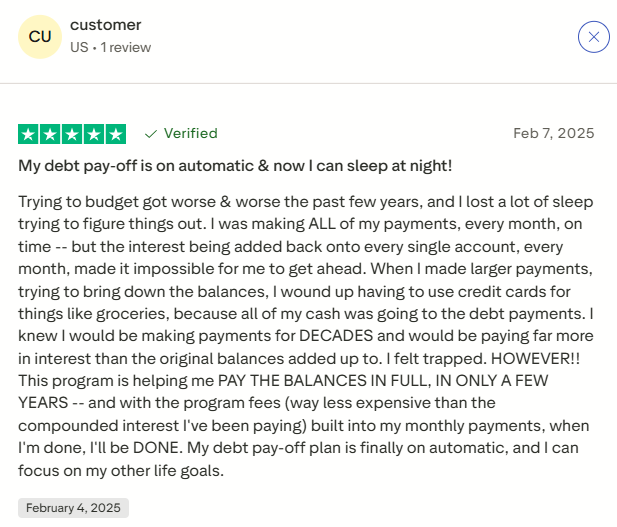

One customer captured the universal frustration: “Trying to budget got worse & worse the past few years, and I lost a lot of sleep trying to figure things out. I was making ALL of my payments, every month, on time—but the interest being added back each month was keeping me in a never-ending cycle.”

This is the debt trap: you’re doing everything “right” like making payments and staying current but you’re still losing ground. The math works against you when interest compounds faster than you can pay the principal.

The counterintuitive solution:

Taking out a new loan (consolidation) to pay off existing debt works when:

- The new loan has a significantly lower interest rate

- Fixed payments replace the minimum payment treadmill

- Clear timeline replaces indefinite debt relationship

- Structure prevents debt reaccumulation

It’s not “more debt” but better-structured debt that actually decreases instead of perpetually renewing.

Real Outcome #1: From Endless Treadmill to a Clear Finish Line

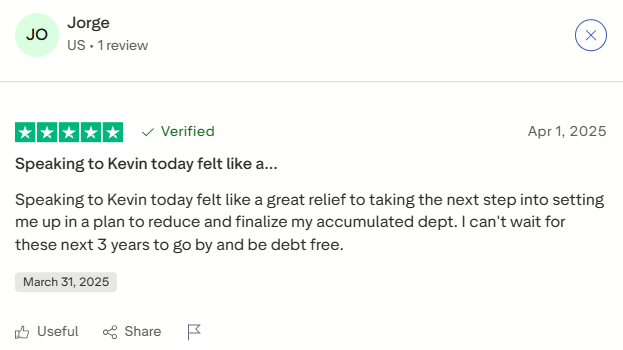

LendWyse customer Jorge’s experience shows the first major outcome: “Speaking to Kevin today felt like a great relief to taking the next step into setting me up in a plan to reduce and finalize my accumulated dept. I can’t wait for these next 3 years to go by and be debt free!”

Before consolidation:

- Timeline: Unknown, likely 15-20 years at minimum payments

- Feeling: Trapped in an endless cycle

- Progress: Barely visible despite consistent payments

- Psychological state: Hopeless, stressed

After consolidation:

- Timeline: Exactly 3 years to debt freedom

- Feeling: Relief and hope

- Progress: Clear countdown with visible milestones

- Psychological state: Motivated, empowered

Is this outcome worth it?

Ask yourself: Would you rather spend 15 uncertain years hoping to eventually become debt-free, or 3 definite years with a clear finish line?

The answer becomes obvious when you stop thinking about “taking on debt” and start thinking about “structured elimination.”

Real Outcome #2: Immediate Psychological Relief

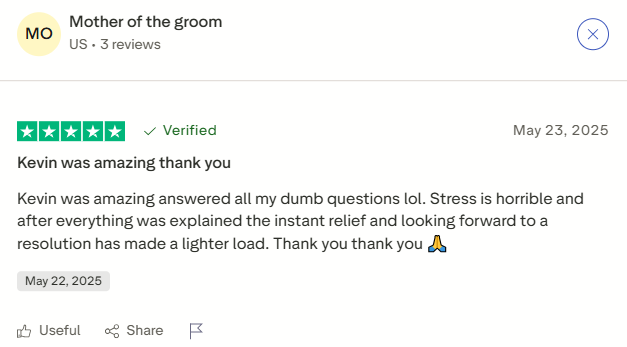

Mother of the groom captured this outcome: “Stress is horrible, and after everything was explained the instant relief and looking forward to a resolution has made a lighter load.”

Notice the language: “instant relief,” “lighter load.” This psychological shift happens immediately, not when the debt is paid off, but when you finally understand your path to freedom.

The stress of unmanaged debt:

- Constant anxiety about juggling multiple payments

- Fear of missing due dates across different cards

- Shame about your financial situation

- Sleepless nights worrying about the future

- Avoiding thinking about money because it’s overwhelming

The relief after consolidation:

- One payment date to remember

- Clear understanding of exactly what you owe

- Timeline you can visualize

- Plan you can execute

- Hope replacing despair

Another customer reinforced this: “Everyone I spoke with were very understanding, helpful and treated me with such respect. We all encounter some sort of hardship and don’t want to be judged for decisions that were made.”

Is psychological relief worth it?

Mental health has financial value. Stress impairs decision-making, reduces work performance, damages relationships, and creates health problems. The immediate psychological relief from consolidation often produces downstream benefits beyond just the financial savings.

Real Outcome #3: Dramatic Interest Savings

Let’s examine the real financial impact using typical scenarios:

Scenario: $15,000 in credit card debt

Without Consolidation (Minimum Payments):

- Average APR: 22%

- Monthly payment: ~$450 (minimum)

- Timeline: 15+ years

- Total paid: $30,000+

- Total interest: $15,000+

With Consolidation (12% Personal Loan, 5 Years):

- APR: 12%

- Monthly payment: $334 (fixed)

- Timeline: Exactly 5 years

- Total paid: $20,040

- Total interest: $5,040

Net outcome:

- Save: $10,000 in interest

- Save: 10+ years of payments

- Reduce: Monthly payment by $116

- Gain: Definite freedom date

Is saving $10,000 and 10 years worth it?

This isn’t theoretical. These are real numbers from real consolidation outcomes. The question isn’t whether consolidation is worth it but whether throwing away $10,000 and a decade of your life is worth avoiding consolidation.

Real Outcome #4: Simplified Financial Life

Multiple customers mentioned the relief of simplification:

Linda Gilbreath noted: “Everyone I spoke with was kind and courteous. Very refreshing. My wait time was not long. Taj was extremely helpful and patient. I felt comfortable discussing my situation with him.”

That comfort “discussing my situation” partly comes from finally having a simplified situation to discuss rather than the complex juggling of multiple cards.

Before consolidation complexity:

- Chase Visa: $4,200 at 19.99%, due on the 15th

- Capital One: $3,800 at 24.99%, due on the 3rd

- Discover: $2,900 at 21.99%, due on the 22nd

- Citi: $4,100 at 23.49%, due on the 8th

- Total: Four different due dates, four different minimums, constant mental tracking

After consolidation simplicity:

- One personal loan: $15,000 at 12%, due on the 1st

- Total: One due date, one amount, mental peace

Is simplification worth it?

The cognitive load of managing multiple debts is exhausting. That mental energy could be used for:

- Career advancement

- Better parenting

- Relationship building

- Creative pursuits

- Actually enjoying life

Simplification frees mental bandwidth that debt complexity consumed.

Real Outcome #5: Credit Score Improvement

Many people avoid consolidation, fearing credit score damage. But the actual outcome often surprises them:

How consolidation typically affects credit:

Short-term (First 3 Months):

- Small dip from hard inquiry (5-10 points)

- Temporary impact from a new account

Medium-term (3-6 Months):

- Significant improvement from lowered credit utilization

- Paying off credit cards drops utilization to 0%

- This often outweighs the inquiry impact

- Net result: Credit score is often higher than before

Long-term (12+ Months):

- On-time loan payments build a positive history

- Diverse credit mix (installment loan + credit cards)

- Continued utilization benefit if cards stay open with zero balances

- Net result: Substantially improved credit

Is the temporary dip worth long-term improvement?

A 10-point temporary dip that leads to a 50-100 point improvement over 18 months is absolutely worth it, especially if the alternative is credit score stagnation while carrying high balances.

Real Outcome #6: Breaking the Reaccumulation Cycle

David North’s experience shows the mindset shift: “Well, I was a little skeptical at first, but he made a lot of sense in what he was saying as far as me trying to pay two cards off and going with beyond in order to make everything work out very comfortably.”

That shift from “trying to pay two cards off” (DIY approach, likely while still using cards) to a structured program represents breaking the reaccumulation cycle.

The reaccumulation trap:

- Pay down the credit card balance

- Feel like you have “available credit”

- Use card for “emergency” or “good deal”

- Balance goes back up

- Repeat indefinitely

How consolidation breaks the cycle:

- Consolidation loan pays off credit cards

- Cards closed or severely restricted

- No available credit to tempt spending

- Forced to budget within income

- Loan balance only goes down, never up

Grace D appreciated this structured approach: “Kameel was the reason I was even open about this company. Not only did he take the time to help me understand the whole process, he was very kind about it. His expertise was obviously on point and there were no questions he was unable to answer.”

Understanding “the whole process” is what makes consolidation work long-term.

Is forced discipline worth it?

If your track record shows difficulty with credit card discipline, consolidation’s forced structure isn’t a punishment but a tool that works with human psychology rather than requiring superhuman willpower.

Real Outcome #7: Regaining Financial Control

Tamaira Barnes-Hart’s emotional response reveals this outcome: “I can’t even thank you enough for taking care of my debt….I should of done this along time ago. I’m so happy, this made my day!!!!”

That joy comes from regaining control after years of feeling controlled by debt.

Feeling controlled by debt:

- Debt dictates your decisions

- Can’t plan for the future because the present is overwhelming

- Constant reaction to financial emergencies

- Life feels on hold until the debt is handled

- Every financial decision is filtered through the debt burden

Regaining control through consolidation:

- You dictate the terms (choosing loan, timeline, payment amount)

- Can plan the future because the present is structured

- Proactive approach with clear milestones

- Life resumes while systematically eliminating debt

- Financial decisions made from a position of clarity

Is regaining control worth it?

When debt controls you, every aspect of life suffers — career choices, relationship decisions, mental health, and even physical health. Regaining control through consolidation isn’t just about money but reclaiming your life.

When Consolidation ISN’T Worth It

To maintain credibility, let’s acknowledge when consolidation isn’t worth pursuing:

Skip consolidation if:

- You can pay off debt in under 12 months with focused effort

- Consolidation overhead not worth it for short timelines

- Just buckle down and eliminate debt quickly

- Consolidation rates aren’t meaningfully better

- If you can only qualify for rates similar to current cards

- Savings don’t justify the hassle

- You haven’t addressed spending behavior

- Consolidation without behavior change just delays problems

- Will likely end up with loan payments PLUS new credit card debt

- Debt is so overwhelming that even consolidation won’t work

- If debt exceeds annual income significantly

- Debt settlement or bankruptcy might be more appropriate

Amy Barnard appreciated being treated with dignity: “I wasn’t made to feel like I was an awful person, very understanding and personable.”

That understanding includes an honest assessment of when consolidation fits and when alternatives make more sense. Reputable services don’t force consolidation on everyone but recommend what actually works.

The Alternatives When Consolidation Isn’t the Answer

JANET RANK’s experience shows flexibility: “Maurice was so helpful and kind. I did not qualify for a personal loan and he helped me understand what alleviate could do to help me. And for the first time in a while, I feel very positive about the process.”

When traditional consolidation doesn’t fit:

Debt Management Plans (DMPs):

- Negotiate lower rates without new loans

- Single payment through a counseling agency

- Good for those who can’t qualify for consolidation rates

Debt Settlement:

- Negotiate to pay less than owed

- For overwhelming debt situations

- Significant credit impact but path to freedom

Bankruptcy:

- Last resort for truly unmanageable debt

- Clean slate but severe consequences

- Sometimes the most responsible choice

Is it worth it to explore alternatives?

If traditional consolidation isn’t worth it for your situation, having a service that explores alternatives rather than just rejecting you is absolutely worth the conversation.

The Total Value Calculation

When determining if consolidation is worth it, consider the complete picture:

Financial Outcomes:

- Interest savings: Often $5,000-$15,000

- Time savings: 5-15 years to freedom

- Monthly cash flow: Often $50-200 more available

Psychological Outcomes:

- Immediate stress reduction

- Hope replacing despair

- Clear goals replacing uncertainty

- Control replacing helplessness

Practical Outcomes:

- Simplified financial management

- Better credit score trajectory

- Forced discipline preventing reaccumulation

- Mental bandwidth freed for other priorities

Relationship Outcomes:

- Reduced financial stress on partnerships

- Ability to make joint financial plans

- Removing money as a constant source of conflict

Opportunity Outcomes:

- Career decisions not limited by debt

- Ability to save for important goals

- Freedom to invest in yourself

- Life not on hold indefinitely

Total value: Transformative life change

The Decisive Question

Paula Siwek captured what makes consolidation worthwhile: “ALEN is a human being, and made me feel informed and comfortable. I didn’t know what expect from our conversation, and he made the terms clear and realistic.”

“Clear and realistic” expectations determine whether consolidation is worth it:

Ask yourself:

- “Will this actually reduce my total cost?”

- If yes by significant amount: Worth it

- If marginal: Maybe not

- “Will this give me a clear path I can stick to?”

- If yes: Worth it

- If unrealistic payments: Not worth it

- “Will this reduce stress and improve quality of life?”

- If yes: Worth it beyond just finances

- If adds complexity: Not worth it

- “Am I ready to change spending behavior?”

- If yes: Consolidation can work

- If no: Won’t be worth it even if numbers work

- “What’s my alternative?”

- If the alternative is 15+ years of minimum payments: Consolidation worth it

- If the alternative is paying off quickly anyway: Maybe not needed

The worth isn’t universal. It’s personal to your specific situation.

The Timing Question: Is Now the Right Time?

One customer expressed regret: “I should have done this a long time ago.”

What waiting costs:

Every month of delay at 22% credit card interest on $15,000:

- Interest charges: ~$275

- Annual interest: ~$3,300

- Five years waiting: $16,500 in interest

What consolidation provides:

Same debt at 12% over five years:

- Total interest: $5,040

- Savings: $11,460

The math is brutal:

Each year you delay consolidation costs thousands in interest. “Waiting for a better time” or “trying to handle it yourself first” can be the most expensive decision you make.

The Bottom Line: Is It Worth It?

For most people carrying significant credit card debt (over $5,000) with high interest rates (over 18%), debt consolidation is emphatically worth it when:

- You qualify for rates significantly lower than your current debt

- Monthly payments are manageable within your budget

- You’re committed to not reaccumulating credit card debt

- You’ve been stuck in the minimum payment cycle for 12+ months

- You want a clear timeline to debt freedom

The real question isn’t “Is consolidation worth it?”

It’s “Is continuing to pay 2-3x your debt over 15+ years worth avoiding consolidation?”

When framed that way, the answer becomes obvious.

Ready to Discover Your Real Outcomes?

Stop wondering whether debt consolidation is worth it in theory. Discover what it means for your specific situation with actual numbers.

What LendWyse customers discovered:

- Clear timelines replacing endless treadmills

- Thousands saved in total interest

- Immediate psychological relief

- Simplified financial lives

- Hope replacing despair

- Control replacing helplessness

See your actual numbers: timeline to freedom, total savings, monthly payment, real outcomes you can expect. Within one conversation, you’ll know whether consolidation is worth it for your situation — not based on general advice, but on your specific debt, income, and goals.

As thousands have learned, the question isn’t whether consolidation is worth it. It’s whether you’re willing to keep throwing away thousands of dollars and years of your life to avoid finding out.