When you’re struggling with over $10,000 in high-interest credit card debt, the last thing you need is to get scammed by a predatory “debt relief” company that makes your situation worse.

The industry is flooded with operations that overpromise, charge excessive fees, and disappear when you need help most. So how do you separate legitimate debt relief companies from the wolves in sheep’s clothing?

The answer isn’t found in marketing promises or slick websites. It’s found in how companies actually treat real customers during their most vulnerable financial moments.

We’ve analyzed hundreds of verified customer reviews to identify the specific behaviors and characteristics that signal a trustworthy debt relief company.

These aren’t theoretical guidelines but real-world indicators that actual customers used to determine whether they could trust LendWyse with their financial future. Let’s explore what trustworthiness looks like in practice.

Table Of Contents:

Red Flag #1: High-Pressure Sales Tactics (And Why You Won’t Find Them Here)

The Scam Approach: Predatory debt relief companies use aggressive sales tactics designed to pressure you into immediate decisions before you have time to think or research. They create artificial urgency, imply the “deal” will disappear, and make you feel stupid for wanting to think things over.

The Trustworthy Approach: Legitimate companies give you space to breathe, think, and ask questions without pressure.

What Real Customers Experienced:

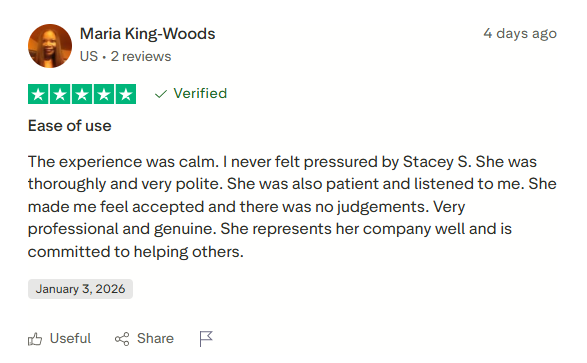

Maria King-Woods wrote:

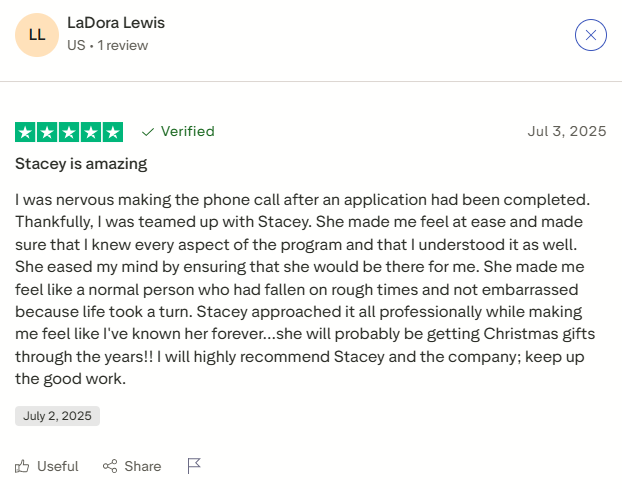

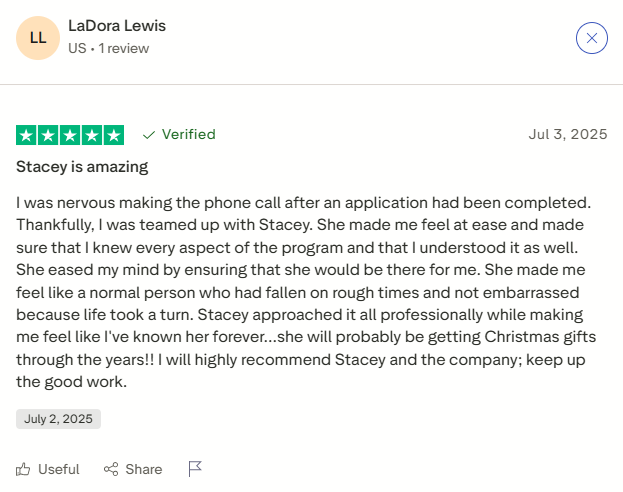

LaDora Lewis shared:

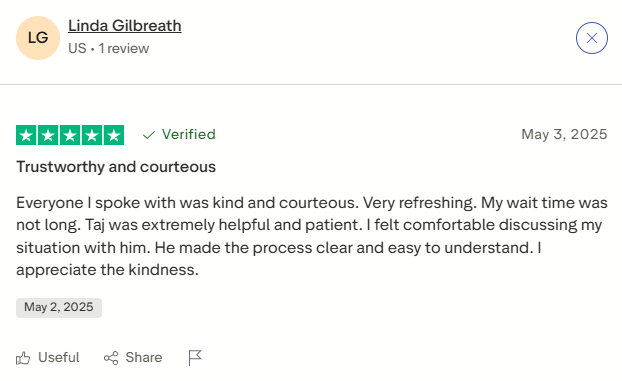

Linda Gilbreath noted:

Trust Indicator: If you feel rushed, pressured, or uncomfortable during initial conversations, that’s a massive red flag. Trustworthy companies understand that you need time to make informed decisions about your financial future.

Red Flag #2: Vague Explanations and Avoiding Questions

The Scam Approach: Predatory companies keep things deliberately vague, avoid direct answers to questions, and use confusing jargon to obscure what’s really happening with your money.

The Trustworthy Approach: Legitimate companies explain everything thoroughly, answer every question patiently, and make sure you understand exactly what you’re signing up for.

What Real Customers Experienced:

Thorough Explanations:

Kate wrote:

“Alen Bates was so incredibly helpful and thorough with everything we discussed! This process, which I was dreading, was extremely easy and stress free because of him. I didn’t have to ask many questions because he explained everything so well.”

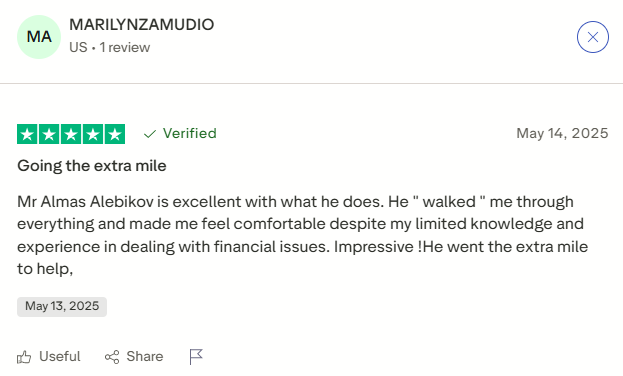

MARILYNZAMUDIO shared:

“Mr Almas Alebikov is excellent with what he does. He ‘walked’ me through everything and made me feel comfortable despite my limited knowledge and experience in dealing with financial issues.”

Patience With Questions:

Mother of the groom wrote:

“Kevin was amazing answered all my dumb questions lol. Stress is horrible and after everything was explained the instant relief and looking forward to a resolution has made a lighter load.”

Nalz stated:

“Almas was so efficient in what he does, very knowledgeable in all aspects…able to answer patiently all my queries….understood my doubts….definitely, he earned my trust and vote of confidence.”

Time Investment:

One customer noted:

“Our specialist, Daniel Frasier, was truly outstanding. Very polite, informative, and patient. He answered all our questions, and spent as much time as needed on the phone with us.”

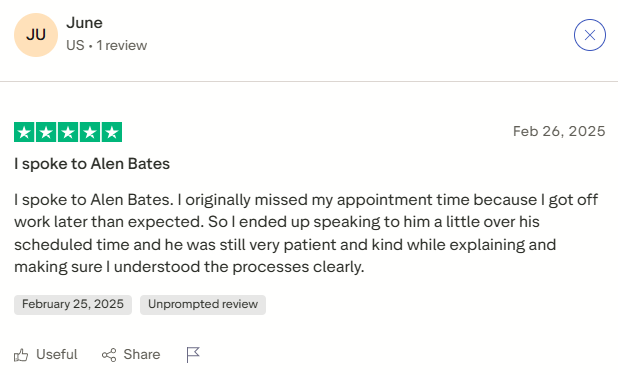

June shared:

“I originally missed my appointment time because I got off work later than expected. So I ended up speaking to him a little over his scheduled time and he was still very patient and helpful even during his over time.”

Trust Indicator: Trustworthy companies invest significant time explaining how programs work, including potential downsides. They encourage questions rather than avoiding them. If representatives seem evasive or rush through explanations, walk away.

Red Flag #3: One-Size-Fits-All Solutions

The Scam Approach: Predatory operations push everyone into the same product regardless of whether it fits their situation because they only care about their commission, not your outcome.

The Trustworthy Approach: Legitimate companies assess your specific situation and recommend solutions that actually fit—even if it means directing you to a different program or admitting you’re not a good fit for their services.

What Real Customers Experienced:

Alternative Solutions When Personal Loans Don’t Fit:

JANET RANK shared:

“Maurice was so helpful and kind. I did not qualify for a personal loan and he helped me understand what alleviate could do to help me. And for the first time in a while, I feel very positive about the process.”

Cosette wrote:

“Due to my credit issues, Taj the representative explained beyond finance. A program that helps with debt reduction and settlement.”

David North noted:

“Well, I was a little skeptical at first, but he made a lot of sense in what he was saying as far as me trying to pay two cards off and going with beyond in order to make everything work out very comfortably.”

Tailored Approaches:

Michael Hamilton appreciated:

“Almas made my experience great. He listened to me and tailored the program to my needs, which was very much appreciated.”

Trust Indicator: If a company only offers one product and pushes it regardless of your situation, they’re not trustworthy. Legitimate debt relief companies recognize that different debt situations require different solutions and will be honest when their primary service isn’t the right fit.

Red Flag #4: Treating You Like a Number Instead of a Person

The Scam Approach: Predatory companies see you as a transaction. They don’t care about your story, your stress, or your dignity. Just whether they can extract money from you.

The Trustworthy Approach: Legitimate companies treat you with respect and compassion, recognizing that people end up in debt for countless legitimate reasons.

What Real Customers Experienced:

Being Treated With Dignity:

Amy Barnard simply stated:

“I wasn’t made to feel like I was an awful person, very understanding and personable.”

Kameel’s customer wrote:

“Kameel was very understanding he didn’t make me feel like I was an irresponsible person. He was very thorough in explained how the process works and what to expect.”

Darrell shared:

“Carmelo was great to work with. He was able to help me understand exactly how the program works because I was under the impression that going this route was bad.”

Compassion and Respect:

Mary noted:

“Alen was my agent and treated me with compassion, respect, and patience. I am compromised with a brain illness that make me vulnerable to financial loss, and Alen’s continual reassurances and non-rushed manner gave me confidence and trust.”

ROBERTO NIEVES wrote:

“Rochelle Hockemeyer was helpful and amazing. She showed understanding, did not feel judge. Had an amazing call and felt comfortable and at ease with everything spoken about.”

Special Accommodations:

Patricia A Valese appreciated:

“This was a great experience because your representative took his time explaining everything to me. He also had much patience since I am hard of hearing.”

Trust Indicator: Trustworthy companies understand that financial difficulties are often caused by circumstances beyond your control like medical emergencies, job loss, divorce, or simply never being taught proper money management. If you feel judged or looked down upon, find a different company.

Red Flag #5: Disappearing After the Sale

The Scam Approach: Predatory companies are all smiles until they get your signature and payment, then they become impossible to reach when you have questions or problems.

The Trustworthy Approach: Legitimate companies maintain communication, follow up on your progress, and remain available to answer questions throughout the process.

What Real Customers Experienced:

Follow-Through:

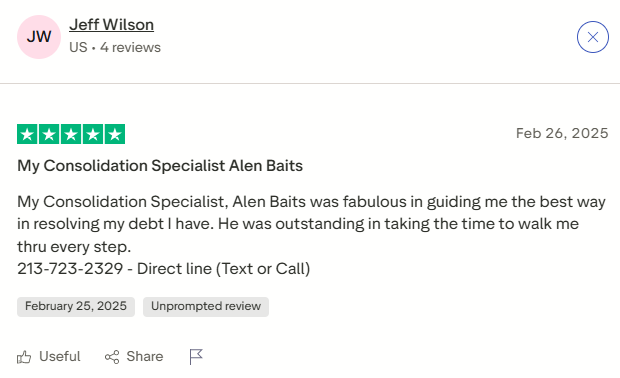

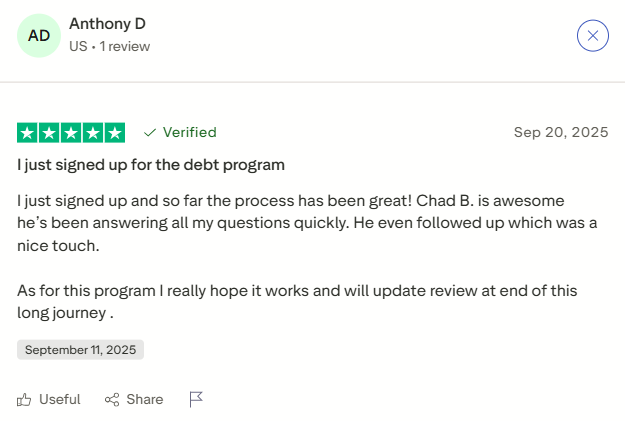

Anthony D wrote:

“I just signed up and so far the process has been great! Chad B. is awesome he’s been answering all my questions quickly. He even followed up which was a nice touch.”

Marc noted:

“Rachel really went over everything and made sure I felt comfortable, gave me additional advice in general with other accounts I may have and how to move forward.”

Continued Support:

CBoss shared:

“I worked with Tony and the initial process was very well detailed a laid out. So I hope everything goes according to plan and I will check back in later once I have been in the plan for some time to give an update. Tony was very good at what he does though.”

Trust Indicator: Look for evidence that the company maintains relationships beyond the initial sale. Check reviews specifically mentioning follow-up communication and continued support. If reviews only cover the sales process with no mention of ongoing service, be cautious.

Red Flag #6: Unrealistic Promises

The Scam Approach: “We’ll eliminate 90% of your debt!” “Fix your credit in 30 days!” “Get out of debt without paying!” If it sounds too good to be true, it is.

The Trustworthy Approach: Legitimate companies provide realistic expectations about what debt relief can and cannot accomplish, including potential downsides.

What Real Customers Experienced:

Clear, Realistic Terms:

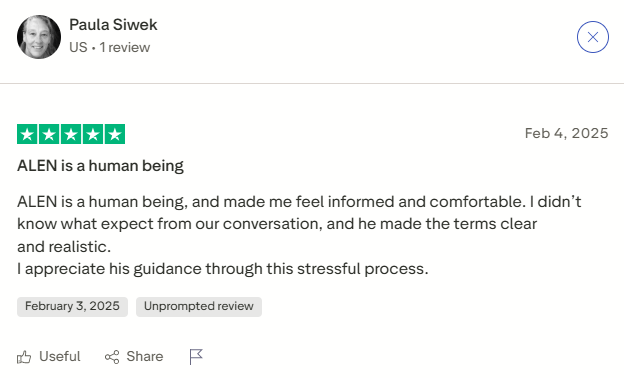

Paula Siwek wrote:

“ALEN is a human being, and made me feel informed and comfortable. I didn’t know what expect from our conversation, and he made the terms clear and realistic.”

Honest Discussions:

Multiple reviewers mentioned representatives explained both benefits and potential drawbacks, helping them make informed decisions rather than painting an unrealistically rosy picture.

Trust Indicator: Be extremely wary of companies making promises that sound miraculous. Debt relief is legitimate but it’s not magic. Trustworthy companies explain realistic timelines, potential credit impacts, and what you’ll need to do to succeed.

The Trust Checklist: Questions to Ask Any Debt Relief Company

Based on real customer experiences with trustworthy services, here are the questions every debt relief company should answer clearly:

About Their Services

“What debt relief options do you offer?”

- Trustworthy answer: Multiple options (personal loans, debt management, settlement) depending on your situation

- Red flag answer: Only one product pushed on everyone

“How do you determine which solution is right for me?”

- Trustworthy answer: Detailed assessment of your debt, income, credit, and goals

- Red flag answer: Vague response or assumption that everyone needs their product

“What are the potential downsides of this approach?”

- Trustworthy answer: Honest discussion of credit impacts, timelines, and requirements

- Red flag answer: Only mentions benefits, avoids discussing drawbacks

About Fees and Costs

“What fees do you charge and when are they due?”

- Trustworthy answer: Clear breakdown of any fees, when they’re charged, and what they cover

- Red flag answer: Evasive responses, upfront fees before any service, or hidden costs

“How much will I save compared to my current situation?”

- Trustworthy answer: Realistic calculations based on your specific debts and rates

- Red flag answer: Exaggerated savings claims without backing them up with math

About The Process

“How long will this process take?”

- Trustworthy answer: Realistic timelines with milestones (typically 2-5 years for most programs)

- Red flag answer: Promises of unrealistically fast debt elimination

“What happens if I can’t make a payment?”

- Trustworthy answer: Clear explanation of consequences and options for hardship

- Red flag answer: Avoiding the question or acting like it’s impossible

“Can I speak with existing clients about their experience?”

- Trustworthy answer: Provides references or directs you to verified review platforms

- Red flag answer: Refuses or makes excuses

About Communication

“Who will I work with throughout this process?”

- Trustworthy answer: Assigned representative or team with direct contact information

- Red flag answer: Vague response about “customer service department”

“How can I reach you if I have questions?”

- Trustworthy answer: Multiple contact methods, reasonable response times

- Red flag answer: Limited contact options, difficult to reach

Verification: How to Research Before You Commit

Don’t just take a company’s word for it. Do your homework:

1. Check Independent Review Platforms

Trustpilot, Google Reviews, Better Business Bureau: Look for patterns in reviews, not just star ratings. Trustworthy companies will have:

- Hundreds of reviews (not just a handful)

- Consistent themes of patience, respect, and clear communication

- Responses to negative reviews showing they address problems

- High percentage of 4-5 star ratings (95%+ for truly excellent companies)

LendWyse’s Trustpilot Profile:

- 4.7 out of 5 stars

- 600+ verified reviews

- 95% are 5-star ratings

- Consistent themes of respectful treatment, thorough explanations, and no pressure

2. Verify Licensing and Credentials

Check if the company is:

- Licensed in your state (if required)

- Member of industry associations (AFCC for credit counseling, IAPDA for debt settlement)

- Subject to regulatory oversight

- Has no major legal actions or FTC complaints

3. Search for Complaints

Google: “[Company Name] complaints” or “[Company Name] scam”

- Look for patterns, not isolated incidents

- Consider the company’s response to complaints

- Check if complaints are resolved or ignored

4. Test Their Initial Interaction

Pay attention to:

- How quickly they respond

- Whether they answer questions directly

- If you feel pressured or comfortable

- Quality of information provided

The Comparison Test: What Sets Trustworthy Companies Apart

Christopher Browning’s review provides a perfect comparison:

“We called about an offer we got in the mail, was not able to get approved for that, so he suggested a consolidation plan, and we have called several other mail offers and no one else bothered to help us.“

This reveals a crucial distinction: many companies in the debt relief space are really just lead generation operations that:

- Pass your information around to multiple companies

- Only help if you fit their exact product criteria

- Disappear if you don’t qualify for their one service

- Use high-pressure tactics to close deals quickly

Trustworthy companies like LendWyse:

- Assess your complete situation before recommending solutions

- Offer multiple pathways depending on what fits

- Continue helping even if you don’t qualify for their primary service

- Take time to ensure you understand and are comfortable

Warning Signs During Initial Contact

Based on what customers didn’t experience with LendWyse (but commonly encountered with predatory operations):

Immediate Red Flags

- Demanding upfront fees before any service is provided

- Refusing to provide information unless you give credit card details

- Guaranteeing specific debt reduction percentages before reviewing your situation

- Claiming they can stop all creditor calls immediately (only bankruptcy does this)

- Pressuring you to stop paying creditors without explaining the consequences

- Making you feel stupid for asking questions or wanting time to think

- Refusing to put terms in writing or send documentation before enrollment

- Using scare tactics about lawsuits or garnishments to pressure quick decisions

Green Flags (Present in LendWyse Reviews)

- Patient explanation of multiple options

- Clear discussion of both benefits and drawbacks

- No pressure to make immediate decisions

- Respectful treatment regardless of debt level or credit score

- Time spent answering every question thoroughly

- Willingness to admit when their service isn’t the right fit

- Providing direct contact information for ongoing support

- Following up and maintaining communication

The Role of Personalization: Why It Matters

One consistent theme across trustworthy debt relief experiences is personalization—representatives taking time to understand your specific situation rather than running through a scripted sales pitch.

Real examples:

Marlon White shared:

“Maryam was very professional and knowledgeable. I felt comfortable sharing my identity information with her. She walked me through everything and I am happy to get the financial ease that I needed at this time.”

Marcia Kettle noted:

“I am not great on my I phone but Shomari was very patient! He answered all my questions! He made a stressful situation somewhat more comfortable.”

Emily Pitman wrote:

“I worked with Ben & Tyrisha; both of them were extremely helpful – thorough, knew all of the answers to my questions, and personable. The process of signing up was incredibly simple and efficient.”

Why personalization signals trustworthiness:

- Shows the company values you as an individual

- Indicates they’re assessing fit rather than just closing sales

- Demonstrates expertise in handling diverse situations

- Builds confidence that recommendations suit your specific needs

Cultural Competence and Accessibility

Trustworthy companies accommodate diverse needs and communication styles:

Language and Communication:

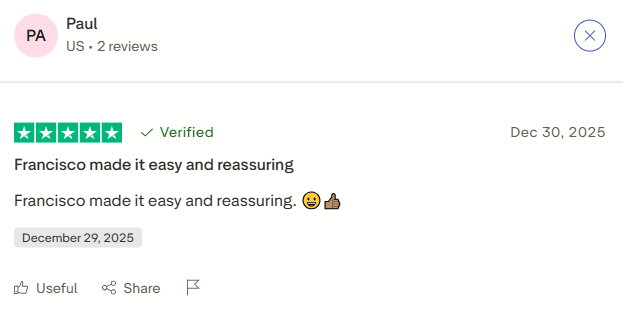

Francisco Dominguez’s customer, Jason, noted:

“Fransisco Dominguez was polite, professional, courteous and very patient. Explained everything in detail and was extremely helpful in helping us understand the process and offered tips on how to move forward.”

Special Needs:

Patricia A Valese mentioned:

“He also had much patience since I am hard of hearing.”

Mary appreciated:

“I am compromised with a brain illness that make me vulnerable to financial loss, and Alen’s continual reassurances and non-rushed manner gave me confidence and trust.”

Trust Indicator: Companies that accommodate diverse communication needs and show patience with customers who need extra time or different explanations demonstrate a genuine commitment to helping everyone, not just “easy” customers.

The Emotional Intelligence Factor

Debt is deeply emotional. Trustworthy companies recognize this and respond with empathy rather than judgment.

Real examples:

Katy Shoemaker wrote:

“Chad was really great to work with. He was kind, empathetic, and described the process so clearly. I appreciate having someone like him help me during this time.”

Another customer shared:

“Everyone I spoke with were very understanding, helpful and treated me with such respect. We all encounter some sort of hardship and don’t want to be judged for decisions that were made.”

Luis’s customer, Erick, noted:

“Luis was a very helpful employee. I never felt talked down to about my financial status and he was very patient throughout the whole process.”

Why emotional intelligence matters:

- Shows the company understands the human side of debt

- Reduces shame and anxiety that prevent people from seeking help

- Creates an environment where you can be honest about your situation

- Indicates the company prioritizes long-term success over quick sales

Making Your Decision: A Framework

When evaluating any debt relief company:

Step 1: Initial Research (Before Contact)

- Check Trustpilot, BBB, Google Reviews

- Look for patterns in customer experiences

- Verify licensing and credentials

- Search for complaints and how they’re resolved

Step 2: Initial Contact (Test the Waters)

- Pay attention to your gut feelings

- Note whether you feel pressured or comfortable

- Assess how thoroughly they answer questions

- Observe if they listen or just pitch

Step 3: Evaluation (Decision Time)

- Do they offer multiple solutions or one product?

- Are explanations clear and realistic?

- Do you feel respected and understood?

- Can you reach them easily for follow-up questions?

Step 4: Verification (Before Committing)

- Get everything in writing

- Verify fees, terms, and timelines

- Confirm you understand the potential downsides

- Ensure you have direct contact information

Step 5: Monitor (After Enrollment)

- Does follow-through match initial promises?

- Can you reach them when you have questions?

- Are they responsive to concerns?

- Do they maintain the same level of service?

The Bottom Line: Trust Your Instincts (Backed by Research)

Trustworthy debt relief companies distinguish themselves through consistent patterns of behavior that real customers experience:

- Patient, pressure-free conversations where you control the pace

- Thorough explanations of how programs work, including potential drawbacks

- Respectful treatment regardless of your debt level or credit situation

- Personalized recommendations based on your specific circumstances

- Multiple solution options rather than one-size-fits-all products

- Continued communication and support throughout the process

- Honest assessments even when it means directing you elsewhere

- Emotional intelligence recognizing the stress and shame associated with debt

As Daniel Braden summarized about his representative:

“Rhonda was absolutely wonderful throughout this whole process. Her customer service is 10 stars, you just don’t give that option.”

When you find a company demonstrating these characteristics consistently across hundreds of customer experiences, you’ve found a trustworthy partner in your journey to financial freedom.

Ready to Experience Trustworthy Debt Relief?

The difference between a predatory debt relief company and a trustworthy one isn’t just about better service. It’s about whether you actually achieve financial freedom or remain trapped in debt with new problems added.

Based on 600+ verified customer reviews, maintaining a 4.7-star rating, LendWyse demonstrates the consistent patterns of trustworthiness that matter when you’re making this critical decision.

Ready to experience what trustworthy debt relief looks like? Connect with LendWyse for a pressure-free consultation about your debt consolidation options.

Get Your Free Consultation at LendWyse.com