Bankruptcy vs Debt Management: Compare Your Options

Compare bankruptcy options to debt management plans with an objective analysis of long-term impacts.

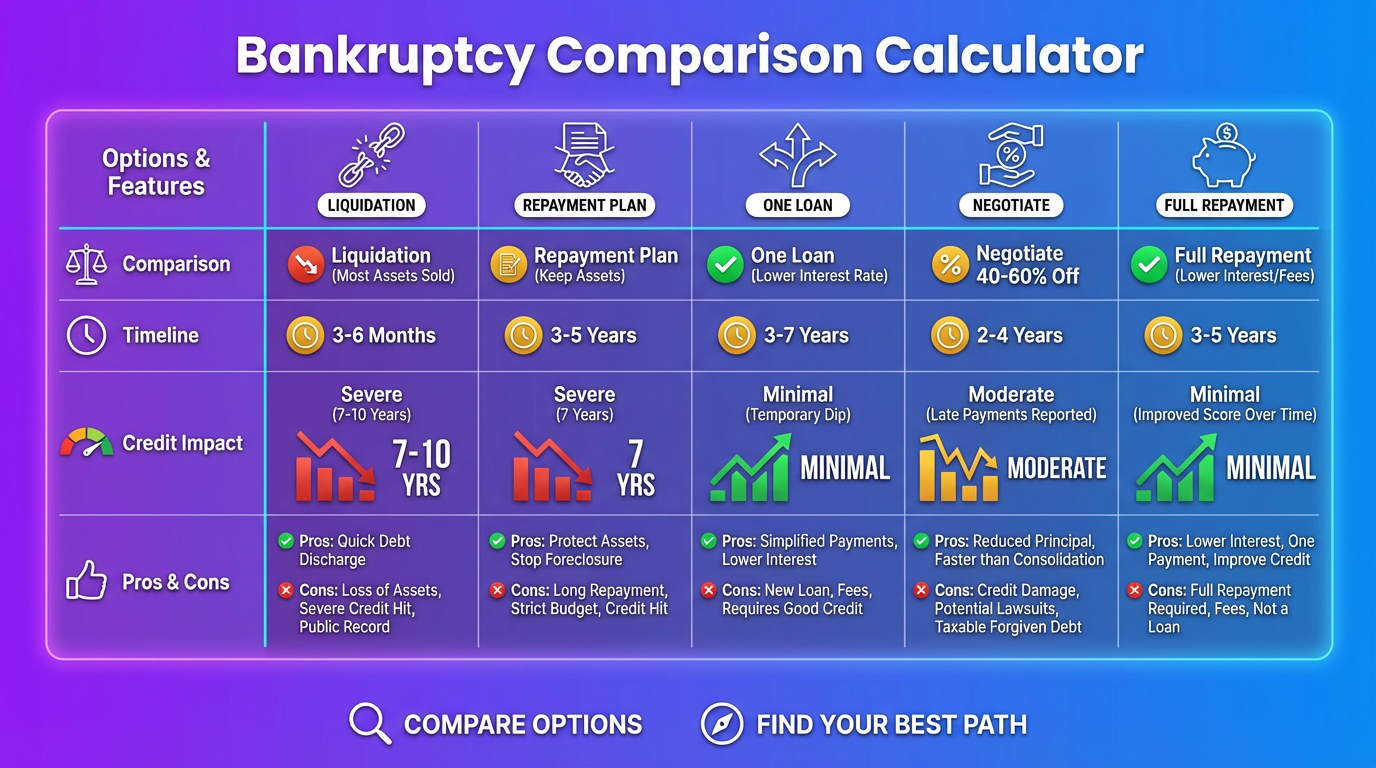

How This Bankruptcy Comparison Calculator Works

Our bankruptcy comparison calculator helps you understand all debt relief options before making a major decision. Compare:

- Chapter 7 bankruptcy – Discharge unsecured debt

- Chapter 13 bankruptcy – Structured repayment plan

- Debt consolidation – Single lower-rate loan

- Debt settlement – Negotiate reduced balances

- Debt management – Nonprofit counseling plan

- DIY payoff – Self-directed strategies

Bankruptcy is serious. Know all your options before deciding.

Understanding Your Options

Quick Comparison

| Option | Debt Eliminated | Timeline | Credit Impact | Cost |

|---|---|---|---|---|

| Chapter 7 | 100% dischargeable | 3-6 months | Severe (7-10 years) | $1,500-$3,500 |

| Chapter 13 | Remainder after plan | 3-5 years | Severe (7 years) | $3,000-$5,000 |

| Consolidation | 0% (pay in full) | 2-7 years | Minimal | Interest + fees |

| Settlement | 40-60% | 2-4 years | Significant (7 years) | 20-25% of settled |

| Debt Management | 0% (pay in full) | 3-5 years | Moderate | $25-$75/month |

| DIY Payoff | 0% (pay in full) | Varies | None/positive | $0 (just debt) |

When Each Option Applies

Chapter 7 may apply if: – Income below state median (means test) – Unsecured debt is overwhelming – Little to no assets to protect – No ability to repay meaningful amount

Chapter 13 may apply if: – Income above means test but struggling – Want to keep home/car – Can afford partial repayment – Need time to catch up on secured debt

Consolidation may apply if: – Credit score 650+ (for decent rates) – Steady income to make payments – Debt is manageable with better terms – Want to preserve credit

Settlement may apply if: – 90+ days delinquent on accounts – Lump sum available (or can save it) – Willing to accept credit damage – Debt too high but not bankruptcy-worthy

Debt Management may apply if: – Need structure and accountability – Want to pay in full at reduced rates – Multiple creditors to manage – Credit damage already occurred

Debt Relief Examples: Comparing Options

Example 1: $35,000 Credit Card Debt on $50,000 Income

Scenario: Single person, no assets, no home equity, overwhelmed.

Option Comparison:

| Option | Est. Payment | Timeline | Total Cost | Credit Impact |

|---|---|---|---|---|

| DIY (avalanche) | $700/mo | 7.5 years | $63,000 | None |

| Consolidation | $700/mo | 5 years | $46,200 | Minimal |

| Debt Management | $700/mo | 4 years | $36,400 | Moderate |

| Settlement | Lump sums | 3 years | $24,500 | 7 years |

| Chapter 7 | $3,000 | 4 months | $3,000 | 7-10 years |

Analysis: – DIY: Possible but 7+ years is exhausting – Consolidation: Requires 680+ credit score – Debt Management: Good middle ground – Settlement: Cheaper but credit destroyed – Chapter 7: Fastest reset but severe consequences

For this scenario: Debt management or consolidation if credit allows. Chapter 7 if truly no other option.

Example 2: $80,000 Debt on $90,000 Household Income

Scenario: Married couple, own home (mortgage current), want to keep house.

Option Comparison:

| Option | Monthly | Timeline | Total Cost | Keep Home✓ |

|---|---|---|---|---|

| DIY | $1,500/mo | 7 years | $126,000 | Yes |

| Consolidation | $1,500/mo | 5 years | $92,400 | Yes |

| Debt Management | $1,400/mo | 5 years | $84,000 | Yes |

| Settlement | Lump/monthly | 4 years | $56,000 | Risk |

| Chapter 13 | $1,200/mo | 5 years | $72,000 | Yes |

| Chapter 7 | N/A | N/A | N/A | Possibly not |

Analysis: – Chapter 7: Likely don’t qualify (income too high) + home at risk – Chapter 13: Keeps home, structured plan, severe credit impact – Debt Management: Similar cost to Ch. 13, less credit damage – Consolidation: If credit allows, best option

For this scenario: Consolidation first choice, debt management second, Chapter 13 if those fail.

Example 3: $25,000 Debt, Already Delinquent

Scenario: Lost job, now employed again, 6+ months behind on payments.

Option Comparison:

| Option | Reality Check |

|---|---|

| DIY | Hard to restart accounts; collectors calling |

| Consolidation | Credit too damaged to qualify |

| Debt Management | Can stop collections, negotiate rates |

| Settlement | Accounts already delinquent; good timing |

| Chapter 7 | Clean slate but bankruptcy on record |

For this scenario: Settlement or debt management most realistic. Credit already damaged, so additional impact less severe.

Settlement calculation: – Original debt: $25,000 – Settlement (50%): $12,500 – Settlement fees (20%): $2,500 – Total cost: $15,000 (vs. $25,000+)

Example 4: $150,000 Medical Debt, Limited Income

Scenario: Disabled, $28,000 annual income, massive medical bills.

The Reality: – DIY payoff at $500/month: 25+ years – Income too low for meaningful repayment – No assets to protect – Qualify for Chapter 7

Chapter 7 Analysis:

| Factor | Assessment |

|---|---|

| Means test | Pass (income below median) |

| Asset protection | All assets exempt |

| Dischargeable debt | 100% of medical debt |

| Timeline | 4-6 months |

| Cost | $1,500-$2,000 (legal fees) |

| Credit impact | 7-10 years |

For this scenario: Chapter 7 bankruptcy is designed for exactly this situation. Medical debt is the #1 cause of bankruptcy, and the system exists to provide relief.

Example 5: $45,000 Debt, Business Owner

Scenario: Small business owner, variable income, business debt mixed with personal.

Complicating Factors: – Business assets to protect – Variable income harder to budget – Some debt may be business-related – Future credit needs for business

Option Comparison:

| Option | Business Impact |

|---|---|

| DIY | No impact if managed |

| Consolidation | May help cash flow |

| Debt Management | May help; some creditors excluded |

| Settlement | May trigger creditor lawsuits |

| Chapter 7 | May lose business assets |

| Chapter 13 | Can protect business; 3-5 year plan |

For this scenario: Business owners often benefit from Chapter 13 (asset protection) or aggressive DIY/consolidation (preserve credit for business needs).

Deep Dive: Each Option

Chapter 7 Bankruptcy

What it does: Discharges most unsecured debt completely.

Qualification: – Pass “means test” (income below state median) OR – Expenses exceed income (disposable income test)

Process: 1. Credit counseling (required) 2. File petition with court 3. Automatic stay (collections stop) 4. Meeting of creditors (~30 days) 5. Financial management course 6. Discharge (~60 days after meeting)

Timeline: 3-6 months total

What’s discharged: – Credit card debt ✓ – Medical bills ✓ – Personal loans ✓ – Past-due utilities ✓ – Some older taxes ✓

What’s NOT discharged: – Recent taxes ✗ – Student loans (usually) ✗ – Child support/alimony ✗ – Court fines/restitution ✗ – Secured debt (keep paying or surrender) ✗

Credit impact: – Remains on report 7-10 years – Immediate score drop: 130-200+ points – New credit difficult for 2-4 years – Recovery possible within 2-3 years

Chapter 13 Bankruptcy

What it does: Creates 3-5 year repayment plan; remaining unsecured debt discharged.

Qualification: – Regular income required – Unsecured debt under $465,275 – Secured debt under $1,395,875 – Current on tax filings

Process: 1. Credit counseling 2. File petition + repayment plan 3. Automatic stay 4. Confirmation hearing (~45 days) 5. 3-5 years of payments to trustee 6. Discharge after completion

Payment structure: – Disposable income goes to plan – Secured debts paid in full – Priority debts paid in full – Unsecured creditors get remainder – Unpaid unsecured discharged at end

Advantages over Chapter 7: – Keep property (home, car) – Catch up on secured debt arrears – Protect co-signers – No asset liquidation

Credit impact: – Remains on report 7 years – Immediate score drop: 130-200+ points – Demonstrates repayment effort – Mortgage possible 1-2 years after discharge

Debt Consolidation

What it does: Combines debts into single loan with (ideally) lower rate.

Qualification: – Credit score 650+ (for good rates) – Stable income – Debt-to-income ratio acceptable

How it works: 1. Apply for personal loan or balance transfer 2. Use funds to pay off existing debts 3. Make single payment on new loan

Typical terms: – Interest rates: 6-20% (based on credit) – Terms: 2-7 years – Fees: 0-8% origination

Pros: – Single payment convenience – Lower interest rate (usually) – Fixed payoff timeline – Credit score preserved or improved

Cons: – Requires qualifying credit – Temptation to run up paid-off cards – Fees may offset savings – Doesn’t reduce principal

Debt Settlement

What it does: Negotiate with creditors to accept less than full balance.

How it works: 1. Stop paying creditors (become delinquent) 2. Save money in dedicated account 3. Negotiate settlements (typically 40-60%) 4. Pay agreed lump sums

DIY vs. Company:

| Factor | DIY | Settlement Company |

|---|---|---|

| Cost | $0 | 20-25% of enrolled debt |

| Time investment | High | Low |

| Success rate | Varies | 50-60% of enrolled |

| Control | Full | Limited |

Typical timeline: 2-4 years

Tax implications: – Forgiven debt over $600 is taxable income – May receive 1099-C from creditors – Can significantly increase tax bill

Credit impact: – Accounts show “settled” (negative) – Remains 7 years from delinquency – Score drop: 100-150+ points – Recovery possible in 2-3 years

Debt Management Plan (DMP)

What it does: Nonprofit agency negotiates reduced rates; you pay through them.

How it works: 1. Free counseling session 2. Agency contacts creditors 3. Reduced rates/fees negotiated 4. You pay agency; they distribute 5. Complete in 3-5 years

Typical terms: – Interest rates: Reduced to 6-9% – Fees: $25-$75/month to agency – Late fees/over-limit often waived

Pros: – Professional management – Reduced interest rates – Single payment – Pay debt in full – Less credit damage than settlement/bankruptcy

Cons: – Must close credit cards enrolled – Not all creditors participate – Still paying full principal – Monthly fee

Best for: Multiple high-interest accounts, need structure, want to pay in full.

Credit Recovery Comparison

Timeline to Credit Recovery

| Option | Years on Report | Years to Mortgage | Score Recovery |

|---|---|---|---|

| DIY Payoff | N/A (positive) | Now | Best |

| Consolidation | N/A (neutral) | Now | Good |

| Debt Management | 3-5 years | 1-2 years | Moderate |

| Settlement | 7 years | 2-4 years | Slow |

| Chapter 13 | 7 years | 1-2 years after | Moderate |

| Chapter 7 | 7-10 years | 2-4 years after | Slow initially |

Credit Score Impact Estimates

| Event | Approximate Score Impact |

|---|---|

| Chapter 7 filing | -130 to -200+ points |

| Chapter 13 filing | -130 to -200+ points |

| Settled account | -45 to -100 points each |

| 90+ day delinquency | -60 to -100 points |

| Consolidation loan | -5 to -15 points (inquiry) |

| Debt management | -20 to -50 points (closed accounts) |

Frequently Asked Questions

Should I file for bankruptcy✓

Consider bankruptcy if: – Debt exceeds annual income (unsecured) – No ability to pay meaningful amount – Facing lawsuits, garnishment – Already significantly behind – All other options exhausted

Avoid bankruptcy if: – Debt is manageable with adjustments – Can pay off in 3-5 years with effort – Have assets you’d lose – Recent large purchases (fraud concerns) – Need security clearance

Always consult a bankruptcy attorney for advice specific to your situation.

What’s the difference between Chapter 7 and Chapter 13✓

| Factor | Chapter 7 | Chapter 13 |

|---|---|---|

| Timeframe | 3-6 months | 3-5 years |

| Payment | None (except attorney) | Monthly to trustee |

| Asset risk | Some may be liquidated | Keep all assets |

| Income limit | Means test | Must have income |

| Debt discharge | Immediate | After plan completion |

| Best for | Low income, few assets | Homeowners, higher income |

How long does bankruptcy stay on credit report✓

Chapter 7: 10 years from filing date Chapter 13: 7 years from filing date

However: – Individual accounts may fall off at 7 years – Credit rebuilding can start immediately – Mortgage possible 2-4 years post-discharge – Score can recover significantly in 2-3 years

Will bankruptcy stop creditor calls and lawsuits✓

Yes—immediately. The “automatic stay” goes into effect when you file:

- Collections calls must stop

- Lawsuits are paused

- Garnishments stop

- Foreclosure/repossession delayed

Violations: Creditors who violate the stay can be sued.

Can I file bankruptcy on medical debt✓

Yes. Medical debt is unsecured debt and is dischargeable in both Chapter 7 and Chapter 13.

Medical debt facts: – #1 cause of bankruptcy in America – Dischargeable in Chapter 7 (100%) – Included in Chapter 13 plan – No special rules—treated like credit cards

What debts can’t be discharged✓

Non-dischargeable debts include: – Most student loans – Recent income taxes (last 3 years) – Child support and alimony – Court fines and restitution – Debts from fraud or misrepresentation – DUI judgments – HOA fees (post-filing)

Should I use a debt settlement company✓

Pros: – They handle negotiations – Less time investment for you – May get better settlements

Cons: – 20-25% fees (on enrolled debt) – Not all debts get settled – You could DIY for free – Some are scams

If using company: – Research BBB ratings – Understand fee structure – Never pay upfront fees – Keep realistic expectations

Is debt consolidation better than bankruptcy✓

Consolidation is better if: – You can qualify for lower rate – Total debt is manageable – You won’t run up cards again – Credit preservation matters

Bankruptcy may be better if: – Can’t qualify for consolidation – Debt is overwhelming – Would take 10+ years to pay off – Already facing legal action

How do I choose between options✓

Decision framework:

- Can you pay in full with better terms✓ → Consolidation/DMP

- Is debt beyond manageable✓ → Settlement or bankruptcy

- Is income below median✓ → Chapter 7 likely

- Need to protect assets✓ → Chapter 13 likely

- Accounts already delinquent✓ → Settlement possible

Consult professionals: – Free nonprofit credit counseling – Bankruptcy attorney consultation – Financial advisor if applicable

What are alternatives to bankruptcy✓

Before filing bankruptcy, try:

- Negotiate directly – Call creditors, ask for hardship plans

- Debt management – Nonprofit credit counseling

- Balance transfer – 0% APR cards if you qualify

- Personal loan – Consolidate at lower rate

- Debt settlement – DIY negotiation

- Side income – Temporary hustle to attack debt

- Expense cuts – Radical temporary measures

- Sell assets – Clear debt without bankruptcy

What happens to my spouse if I file bankruptcy✓

Depends on the debt:

| Debt Type | Impact on Spouse |

|---|---|

| Joint debts | Spouse remains liable |

| Your debts only | No impact on spouse |

| Community property states | Complex—attorney needed |

Options: – File jointly (both debts discharged) – File individually (only your debts discharged)

Consult an attorney in your specific state.

Can bankruptcy help with student loans✓

Generally no, but exceptions exist:

To discharge student loans, you must prove “undue hardship”: – Cannot maintain minimal living standard – Situation likely to persist – Made good faith effort to repay

This is very difficult but not impossible. Some succeed with: – Permanent disability – Extremely low income – Advanced age with no earning potential

Related Calculators

Explore all your debt options:

- Debt Consolidation Calculator – Compare consolidation savings

- Debt Settlement Calculator – Evaluate settlement option

- Debt Snowball vs Avalanche Calculator – DIY payoff strategies

- Financial Freedom Date Calculator – Time to debt freedom

Important Disclaimer

This calculator and information is for educational purposes only and should not be considered legal advice. Bankruptcy and debt relief options have significant legal and financial implications. Always consult with a qualified bankruptcy attorney and/or nonprofit credit counselor before making decisions about your debt.

Free resources: – Nonprofit credit counseling: NFCC.org – Bankruptcy information: USCourts.gov – Legal aid: LawHelp.org