Family Impact Calculator: How Debt Affects Your Loved Ones

See how debt affects your family's financial future, from college savings to retirement.

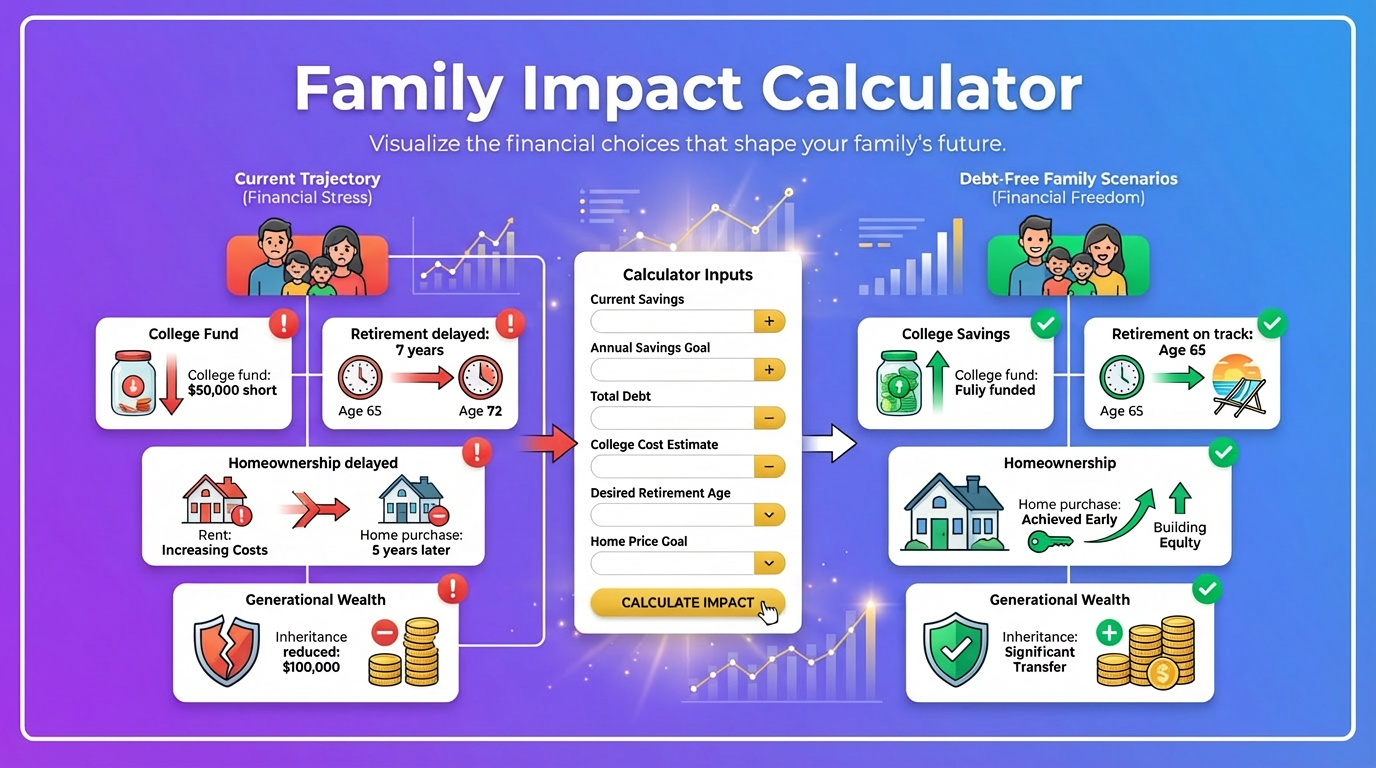

How This Family Impact Calculator Works

Our family impact calculator shows how debt affects your entire family’s financial future. See:

- Children’s education impact – College savings lost to interest

- Retirement timeline – Years delayed by debt

- Homeownership delay – How debt postpones buying

- Generational wealth – What you could pass on instead

- Quality of life – Experiences foregone

Debt doesn’t just affect you. It affects everyone you love.

The Generational Cost of Debt

How Debt Transfers Through Generations

The wealth gap compounds over time:

| Family A (Debt-Free) | Family B (Carrying Debt) |

|---|---|

| Invests $500/month | Pays $500/month to creditors |

| After 30 years: $745,000 | After 30 years: $0 (just debt-free) |

| Passes wealth to children | Passes no wealth (maybe debt habits) |

| Children start ahead | Children start at zero |

| Grandchildren inherit | Grandchildren inherit nothing |

The gap widens with each generation.

What Research Shows

- Children of families with debt have lower academic achievement

- Parental debt stress affects children’s emotional development

- Financial habits are learned—debt patterns often repeat

- Generational wealth is the #1 predictor of economic success

Family Impact Examples: Real Scenarios

Example 1: College Savings Lost to Interest ($35,000 debt)

Scenario: The Martinez family has $35,000 in credit card debt. They have two children, ages 8 and 10.

Current Situation: – Debt: $35,000 at 21% APR – Monthly payment: $800 – Time to pay off: 6.5 years – Total interest: $27,400 – Children’s ages at payoff: 14.5 and 16.5

If They Had No Debt: – $800/month invested at 8% for 6.5 years = $81,000 – That’s $40,500 per child for college

The College Impact:

| Scenario | Child 1 (Age 18) | Child 2 (Age 16) |

|---|---|---|

| With debt | $0 saved | $12,800 saved (2 years) |

| Without debt | $52,000 saved | $81,000 saved |

| Difference | $52,000 | $68,200 |

Combined family education impact: $120,200

Result: Both children may need student loans, perpetuating debt to the next generation.

Example 2: Retirement Delay ($50,000 debt)

Scenario: The Johnsons are 45 with $50,000 in debt and want to retire at 65.

Current Reality: – Debt: $50,000 at 15% (mix of cards and loans) – Monthly payment: $1,000 – Years to payoff: 7 years (age 52) – Retirement contributions possible after debt: 13 years

If They Were Debt-Free Today: – Could invest $1,000/month for 20 years – At 8% return: $589,000

With Debt First: – Invest $1,000/month for 13 years (after debt paid) – At 8% return: $270,000

The Retirement Gap:

| Metric | Debt-Free Now | Pay Debt First |

|---|---|---|

| Years investing | 20 | 13 |

| Total invested | $240,000 | $156,000 |

| Investment value at 65 | $589,000 | $270,000 |

| Difference | — | $319,000 |

Impact: 7 years of debt costs $319,000 in retirement funds.

To match the debt-free scenario, the Johnsons would need to: – Work 5-7 extra years, OR – Invest $2,200/month (if possible) after debt is paid

Example 3: Homeownership Delay ($28,000 debt)

Scenario: Sarah and Mike, age 30, want to buy a home but have $28,000 in debt.

The Debt Burden: – Debt: $28,000 at 18% APR – Monthly payment: $650 – DTI ratio: Too high to qualify for mortgage – Time to pay off: 6 years

Homeownership Timeline:

| Without Debt | With Debt |

|---|---|

| Could buy home at 30 | Must wait until 36 |

| Start building equity | Rent for 6 more years |

| Home appreciates | Miss appreciation |

| Mortgage paid at 60 | Mortgage paid at 66 |

Financial Impact:

| Factor | Without Debt | With Debt | Difference |

|---|---|---|---|

| Rent paid (6 years) | $0 | $97,200 | -$97,200 |

| Equity built (6 years) | $45,000 | $0 | +$45,000 |

| Home appreciation (6 years at 4%) | $52,000 | $0 | +$52,000 |

| Net position | +$97,000 | -$97,200 | $194,200 |

6 years of debt costs nearly $200,000 in homeownership benefits.

Example 4: Family Experiences Foregone ($22,000 debt)

Scenario: The Williams family has two kids (ages 6 and 9) and $22,000 in debt.

What They’re Missing:

| Experience | Cost | Frequency | Value |

|---|---|---|---|

| Family vacation | $4,000 | Annual | $4,000/year |

| Summer camp | $1,500 | Annual per child | $3,000/year |

| Sports/activities | $1,200 | Annual per child | $2,400/year |

| Weekend trips | $400 | 4/year | $1,600/year |

| Birthday parties | $500 | Per child | $1,000/year |

| Total foregone | — | — | $12,000/year |

Over 5 Years of Debt Repayment: – Family vacations missed: 5 – Camp sessions missed: 10 – Sports seasons missed: 10 – Weekend trips missed: 20 – Birthday celebrations scaled back: 10

Children ages during debt: – Child 1: Ages 6 → 11 (key memory-forming years) – Child 2: Ages 9 → 14 (last years before teen independence)

The priceless cost: Memories not made, bonding not experienced, childhood moments lost.

Example 5: Generational Wealth Transfer

Scenario: Two identical families diverge based on debt decisions at age 30.

Family A: Stays Debt-Free – No consumer debt – Invests $600/month – Buys home at 30, paid off at 55 – Retires at 62 with $1.2M

Family B: Carries Debt – $40,000 consumer debt at various times – Pays interest instead of investing – Delays home purchase to 38 – Retires at 67 with $400,000

What Each Family Passes On:

| At Death (Age 85) | Family A | Family B |

|---|---|---|

| Home equity | $650,000 | $450,000 |

| Investment accounts | $2,800,000 | $600,000 |

| Life insurance | $500,000 | $100,000 |

| Debts | $0 | $25,000 |

| Net to children | $3,950,000 | $1,125,000 |

The Generational Gap: $2,825,000

For grandchildren: – Family A’s grandchildren: Receive $200,000 each (8 grandchildren) – Family B’s grandchildren: Receive $56,000 each (8 grandchildren)

Starting position for the 3rd generation differs by $144,000 per person.

The Ripple Effects of Debt

Impact on Children

Short-Term Effects:

| Impact Area | How Debt Affects It |

|---|---|

| Parental stress | Children sense and absorb it |

| Household arguments | Increase with financial strain |

| Activities/experiences | Reduced due to budget |

| Academic focus | May decline with home stress |

| Social activities | Limited by budget constraints |

Long-Term Effects:

| Impact Area | How Debt Affects It |

|---|---|

| Financial education | Learn from observation |

| College support | Less available |

| First car/apartment | Parents can’t help |

| Wedding contribution | May not be possible |

| Home down payment | No parental assistance |

Impact on Marriage/Partnership

Statistics: – Money is #1 topic couples argue about – Couples with debt are 2x more likely to divorce – 36% of debt-related divorces cite amount as primary factor – 54% hid purchases from partner due to debt stress

Relationship Costs:

| Stage | Potential Cost |

|---|---|

| Increased arguments | Relationship quality |

| Therapy/counseling | $2,000-$10,000 |

| Separation expenses | $5,000-$20,000 |

| Divorce (if it goes there) | $15,000-$50,000 |

| Asset division | 50% of everything |

Impact on Extended Family

| Situation | Impact |

|---|---|

| Can’t help aging parents | They may struggle |

| Can’t contribute to family events | Miss milestones |

| Borrow from family | Strain relationships |

| Can’t host gatherings | Miss traditions |

| Can’t travel for events | Miss family moments |

Building Family Wealth Instead

The Alternative Path

What debt payments could become:

| Monthly Payment | 10 Years at 8% | 20 Years at 8% |

|---|---|---|

| $300 | $54,900 | $176,400 |

| $500 | $91,500 | $294,000 |

| $800 | $146,400 | $470,400 |

| $1,000 | $183,000 | $588,000 |

These amounts could fund: – Full college education – Home down payment assistance for children – Family vacation fund – Emergency security – Retirement supplement

Creating Generational Wealth

Keys to breaking the debt cycle:

- Get debt-free – Make it the #1 priority

- Stay debt-free – Build habits that prevent recurrence

- Build savings – Create family security

- Invest consistently – Grow wealth over time

- Teach children – Pass on good habits

- Give strategically – Help next generation start ahead

Frequently Asked Questions

How does parental debt affect children✓

Direct effects: – Less money for activities, experiences, education – Exposure to parental stress and arguments – Learning financial habits (good or bad) by observation – Less help available for major life milestones

Indirect effects: – Academic performance may suffer from home stress – Emotional development affected by family tension – Self-esteem impacted by “can’t afford” messages – Future financial behaviors shaped by childhood experience

Research shows these effects can last into adulthood.

Will my debt affect my child’s financial aid✓

For federal financial aid (FAFSA): – Parent income matters, not parent debt – Your debt doesn’t directly help your child qualify – But debt payments reduce savings you could have

For institutional aid: – Some schools consider family assets – Debt reduces net assets – May slightly help, but not enough to justify debt

Bottom line: Don’t think of debt as a financial aid strategy. The lost savings cost more than any aid benefit.

How much should I save for each child’s education✓

General guidelines:

| Education Goal | 18-Year Savings Needed | Monthly Savings |

|---|---|---|

| Community college | $25,000 | $80 |

| State university | $80,000 | $260 |

| Private university | $200,000 | $650 |

| Full ride supplement | $30,000 | $100 |

Even small amounts help: $100/month for 18 years = $48,000 at 8% return.

Every dollar not going to debt interest could go to education.

Should I pay off debt or save for kids’ college✓

Generally: Pay off high-interest debt first.

Why: – 20% debt interest > 8% investment return – Kids can get loans/scholarships; you can’t borrow for retirement – Reducing debt reduces stress (benefiting whole family) – Once debt-free, you can catch up on savings

Exception: If employer offers 529 matching, get the match while paying debt.

How does debt delay retirement✓

Every year paying debt: – Is a year not investing – Loses compound growth – Pushes retirement date later

Example: $500/month to debt vs. investing

| Scenario | At Age 65 | Retirement Gap |

|---|---|---|

| Invest from 35 | $745,000 | — |

| Start at 40 (5yr debt) | $475,000 | $270,000 |

| Start at 45 (10yr debt) | $294,000 | $451,000 |

10 years of debt costs $451,000 in retirement funds.

Can debt affect my ability to help adult children✓

Yes—in many ways:

| Life Event | How Debt Limits Help |

|---|---|

| First apartment | No deposit help |

| Car purchase | Can’t co-sign or gift |

| Wedding | Limited contribution |

| Home purchase | No down payment help |

| Grandchildren | Less for college funds |

| Emergencies | Can’t be safety net |

Parents often want to help; debt makes it impossible.

How do I talk to kids about our debt✓

Age-appropriate honesty:

Young children (5-10): – “We’re being careful with money right now” – “We’re saving for important things” – Focus on what you CAN do, not what you can’t

Pre-teens (11-13): – Can understand basic concepts – “We’re working to pay off what we owe” – Teach about interest and savings

Teenagers (14+): – Can understand most details – Use as teaching moment – Share the plan and progress – Involve them in budget discussions

Key: Don’t burden children with adult stress, but don’t hide reality entirely.

Does my debt affect my marriage✓

Statistics say yes: – Money is #1 argument topic – Debt doubles divorce risk – 36% of divorces cite debt amount – 54% hide purchases due to debt stress

Protecting your marriage: – Be transparent about finances – Make decisions together – Create shared goals – Celebrate progress together – Consider financial counseling

What’s the “generational wealth gap”✓

Generational wealth = Assets passed from one generation to the next.

The gap: – Families with wealth pass on average $150,000+ – Families with debt pass on $0 (or actual debt) – Each generation starts further apart – Gap widens over time

Debt prevents wealth building that could change your family’s trajectory for generations.

How do I break the debt cycle in my family✓

Steps to break generational debt patterns:

- Acknowledge the pattern – Recognize learned behaviors

- Get educated – Learn what wasn’t taught

- Make a plan – Written debt payoff strategy

- Execute relentlessly – Prioritize debt freedom

- Build savings – Create family security

- Teach children – Give them what you didn’t have

- Model good behavior – They learn by watching

- Celebrate milestones – Make financial success positive

What experiences are most important for children✓

Research on childhood memories: – Experiences matter more than things – Consistency matters more than extravagance – Presence matters more than presents

High-impact, lower-cost experiences: – Family dinners (free) – Bedtime routines (free) – Nature walks/hikes (free) – Game nights (minimal cost) – Cooking together (food budget) – Reading together (library is free)

The best things for children often don’t cost much—but stress-free parents are invaluable.

Should I feel guilty about debt affecting my family✓

Guilt isn’t helpful, but awareness is.

Reframe: – Past decisions are done – Today’s choices matter – Every payment improves the situation – You’re learning and growing – Your awareness shows you care

What helps: – Focus on the future, not the past – Celebrate progress, not perfection – Forgive yourself – Take action (action reduces guilt) – Remember: you’re doing your best

Related Calculators

Build your family’s financial future:

- Debt Snowball vs Avalanche Calculator – Create your payoff plan

- Compound Interest Loss Calculator – See opportunity cost

- Emergency Fund Calculator – Build family security

- Financial Freedom Date Calculator – Know your debt-free date

This calculator provides estimates based on average costs and returns. Your family’s specific situation may vary. The information is educational and not financial advice.