Personal Loan vs Credit Card: Find the Cheaper Option

Compare the true cost of paying with a personal loan vs credit card.

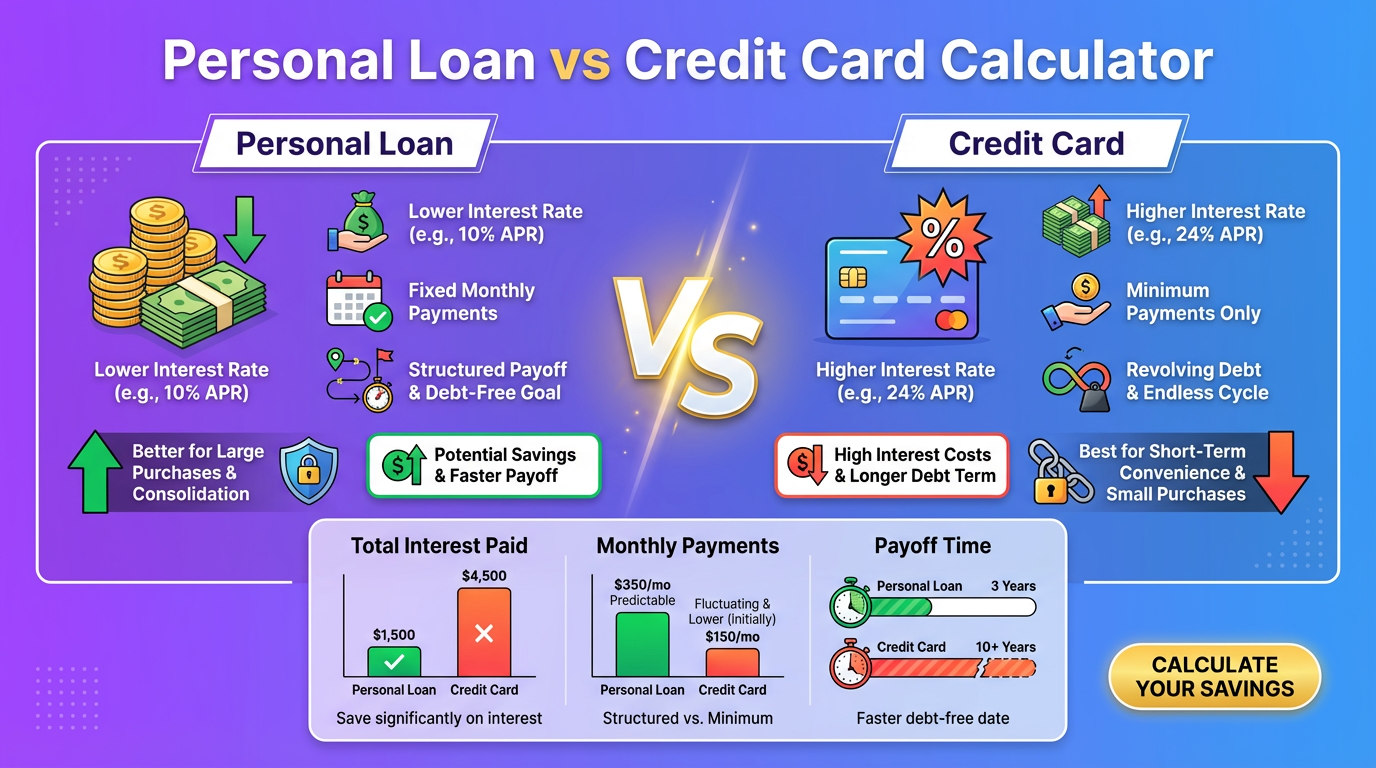

How This Loan vs Credit Card Calculator Works

Our comparison calculator helps you decide between a personal loan and credit card for financing by showing:

- Total cost comparison – Interest paid over the life of each option

- Monthly payment differences – What you’ll pay each month

- Payoff timeline – How long each option takes

- Break-even analysis – When one option becomes better than the other

- Recommendation – Which option makes sense for your situation

Stop guessing. See the actual numbers for your specific situation.

Personal Loans vs Credit Cards: Key Differences

At a Glance

| Factor | Personal Loan | Credit Card |

|---|---|---|

| Interest Rate | 6-36% (fixed) | 15-30% (variable) |

| Payment | Fixed monthly | Flexible minimum |

| Term | 1-7 years | Indefinite |

| Credit Impact | Hard inquiry + new account | Hard inquiry (if new) |

| Funds | Lump sum upfront | Revolving credit |

| Fees | Origination (0-8%) | Annual (some cards) |

| Best For | Large, planned expenses | Smaller, flexible needs |

How Personal Loans Work

- Apply and get approved for specific amount

- Receive lump sum deposited to your account

- Fixed monthly payments over set term (12-84 months)

- Loan closed when paid off

Pros: – Lower interest rates (typically) – Fixed payment = predictable budgeting – Set payoff date – Can’t re-borrow (prevents debt cycling)

Cons: – Origination fees (1-8% common) – Less flexible – Hard inquiry affects credit – Can’t access more if needed

How Credit Cards Work

- Get approved for credit limit

- Spend up to limit as needed

- Pay any amount above minimum

- Revolving credit – can reuse as you pay down

Pros: – Flexible spending – Rewards possible (cash back, points) – 0% intro APR offers available – Use only what you need

Cons: – Higher interest rates – Variable rates can increase – Minimum payments extend debt – Easy to overspend

Personal Loan vs Credit Card Examples: Real Comparisons

Example 1: Home Improvement Project ($15,000)

Scenario: The Smiths need to replace their HVAC system and are comparing financing options.

Option A: Personal Loan – Amount: $15,000 – APR: 10.99% – Term: 48 months – Origination fee: 3% ($450)

| Metric | Value |

|---|---|

| Monthly Payment | $388 |

| Total Interest | $3,174 |

| Total Cost | $18,624 |

| Payoff Date | 48 months |

Option B: Credit Card – Amount: $15,000 – APR: 21.99% – Minimum Payment: 2% or $25 (whichever is greater)

| Payment Strategy | Monthly | Total Interest | Total Cost | Payoff Time |

|---|---|---|---|---|

| Minimums only | Starts $300, decreases | $21,456 | $36,456 | 15+ years |

| Fixed $388 (matching loan) | $388 | $6,234 | $21,234 | 54 months |

| Fixed $500 | $500 | $4,287 | $19,287 | 38 months |

Comparison Summary:

| Factor | Personal Loan | Credit Card (Fixed $388) |

|---|---|---|

| Monthly Payment | $388 | $388 |

| Total Interest | $3,174 | $6,234 |

| Total Cost | $18,624 | $21,234 |

| Savings | $2,610 | — |

Winner: Personal Loan saves $2,610 in interest with same monthly payment.

Example 2: Debt Consolidation ($12,000)

Scenario: Maria has $12,000 in credit card debt at 24.99% APR and is considering a consolidation loan.

Current Situation: – Balance: $12,000 – APR: 24.99% – Monthly payment: $350 – Time to payoff: 49 months – Total interest: $5,067

Option A: Personal Loan – Amount: $12,000 – APR: 12.99% – Term: 36 months – Origination fee: 2% ($240)

| Metric | Value |

|---|---|

| Monthly Payment | $404 |

| Total Interest | $2,304 |

| Total Cost | $14,544 |

| Payoff Date | 36 months |

Option B: Balance Transfer Card – Amount: $12,000 – 0% APR for 18 months – Transfer fee: 3% ($360) – Regular APR after promo: 22.99%

| Scenario | Total Cost | Notes |

|---|---|---|

| Pay off in 18 months ($667/mo) | $12,360 | Best outcome |

| $400/mo (balance remains after promo) | $14,892 | $4,800 remains at 22.99% |

| $350/mo (current payment) | $16,234 | $5,700 remains at 22.99% |

Comparison Summary:

| Option | Total Cost | Monthly Payment | Risk Level |

|---|---|---|---|

| Current (stay) | $17,067 | $350 | Medium |

| Personal Loan | $14,544 | $404 | Low |

| Balance Transfer (pay in 18mo) | $12,360 | $667 | Medium |

| Balance Transfer ($400/mo) | $14,892 | $400 | High |

Winner depends on discipline: – If you can pay $667/mo: Balance transfer saves most – If you prefer certainty: Personal loan is reliable – If minimum budget: Personal loan beats current situation

Example 3: Emergency Medical Bill ($5,000)

Scenario: James received a $5,000 medical bill and needs to finance it.

Option A: Personal Loan – Amount: $5,000 – APR: 14.99% – Term: 24 months – Origination fee: 5% ($250)

| Metric | Value |

|---|---|

| Monthly Payment | $242 |

| Total Interest | $558 |

| Origination Fee | $250 |

| Total Cost | $5,808 |

Option B: Existing Credit Card – Available credit: $6,000 – APR: 19.99%

| Payment Strategy | Monthly | Total Interest | Total Cost | Time |

|---|---|---|---|---|

| Minimum only | Varies | $3,845 | $8,845 | 10+ years |

| Fixed $200 | $200 | $1,024 | $6,024 | 31 months |

| Fixed $242 (matching loan) | $242 | $789 | $5,789 | 25 months |

Option C: Medical Payment Plan – Many providers offer 0% interest payment plans – $5,000 ÷ 24 months = $208/month – Total cost: $5,000

Comparison Summary:

| Option | Total Cost | Monthly | Time |

|---|---|---|---|

| Medical Payment Plan (0%) | $5,000 | $208 | 24 mo |

| Credit Card ($242/mo) | $5,789 | $242 | 25 mo |

| Personal Loan | $5,808 | $242 | 24 mo |

Winner: Medical Payment Plan if available. Otherwise, credit card slightly beats the loan (due to origination fee) if you commit to fixed payments.

Key Insight: For smaller amounts ($5,000 or less), origination fees can make personal loans less attractive.

Example 4: Large Purchase – Furniture ($8,000)

Scenario: The Parkers are furnishing their new home and comparing options.

Option A: Personal Loan – Amount: $8,000 – APR: 11.99% – Term: 36 months – Origination fee: 3% ($240)

| Metric | Value |

|---|---|

| Monthly Payment | $266 |

| Total Interest | $1,336 |

| Total Cost | $9,576 |

Option B: Store Financing (0% for 24 months) – Amount: $8,000 – 0% APR for 24 months – Deferred interest: If not paid in full, ALL interest charged retroactively at 29.99%

| Scenario | Monthly Needed | Total Cost | Risk |

|---|---|---|---|

| Paid in 24 months | $334 | $8,000 | None |

| $100 remaining at month 24 | — | $8,000 + $4,800 retroactive | $12,800 |

Option C: Rewards Credit Card – Amount: $8,000 – APR: 18.99% – Cash back: 2% ($160)

| Payment Strategy | Monthly | Total Interest | Net Cost | Time |

|---|---|---|---|---|

| $266/mo (matching loan) | $266 | $1,698 | $9,538 | 37 mo |

| $334/mo (matching store) | $334 | $1,178 | $9,018 | 28 mo |

Comparison Summary:

| Option | Total Cost | Monthly | Best If… |

|---|---|---|---|

| Store 0% (paid in full) | $8,000 | $334 | Disciplined, can afford $334/mo |

| Personal Loan | $9,576 | $266 | Want lower monthly, guaranteed |

| Credit Card + rewards | $9,018-$9,538 | $266-$334 | Have rewards card, disciplined |

Winner: Store financing IF you’re 100% certain you’ll pay in full. Otherwise, personal loan is safer.

Warning: Deferred interest is a trap. If you’re not certain, avoid it.

Example 5: Wedding Expenses ($20,000)

Scenario: Alex and Jordan need to finance part of their wedding.

Option A: Personal Loan – Amount: $20,000 – APR: 9.99% – Term: 60 months – Origination fee: 2% ($400)

| Metric | Value |

|---|---|

| Monthly Payment | $425 |

| Total Interest | $5,100 |

| Total Cost | $25,500 |

Option B: Multiple Credit Cards – Card 1: $8,000 at 18.99% – Card 2: $7,000 at 21.99% – Card 3: $5,000 at 19.99% – Average APR: ~20%

| Payment Strategy | Monthly | Total Interest | Total Cost | Time |

|---|---|---|---|---|

| Minimums only | Varies | $22,000+ | $42,000+ | 15+ years |

| Fixed $425 (matching loan) | $425 | $10,234 | $30,234 | 70 months |

| Fixed $600 | $600 | $6,123 | $26,123 | 45 months |

Option C: 0% Balance Transfer (post-wedding) – Transfer $20,000 to 0% card – Transfer fee: 3% ($600) – 0% period: 21 months

| Scenario | Monthly Needed | Total Cost |

|---|---|---|

| Paid in 21 months | $952 | $20,600 |

| $600/mo (balance remains) | $600 | ~$23,500 |

Comparison Summary:

| Option | Total Cost | Monthly | Risk |

|---|---|---|---|

| Personal Loan | $25,500 | $425 | Low |

| Credit Cards ($425/mo) | $30,234 | $425 | Medium |

| Balance Transfer (paid in 21mo) | $20,600 | $952 | Medium |

Winner: Balance transfer IF you can afford $952/month. Otherwise, personal loan saves $4,734 over credit cards with same payment.

When to Choose a Personal Loan

Personal Loan Is Better When:

✓ Amount is $5,000+ – Origination fees become proportionally smaller ✓ You want fixed payments – Predictable budgeting ✓ Your credit score qualifies for good rates – Below 12% ✓ You need discipline – Can’t re-borrow on a closed loan ✓ Timeline is 2-5 years – Structured payoff ✓ Current credit card rates are high – 20%+

Personal Loan Advantages

| Advantage | Why It Matters |

|---|---|

| Fixed rate | Know exactly what you’ll pay |

| Set end date | Guaranteed payoff timeline |

| Lower rates | Typically 10-15% less than cards |

| Single payment | Simplifies finances |

| Closed-end | Can’t rack up more debt |

When to Choose a Credit Card

Credit Card Is Better When:

✓ Amount is under $3,000 – Origination fees hurt loan value ✓ 0% intro APR available – Free financing if paid in time ✓ You’ll pay quickly – Under 12 months ✓ You want rewards – Cash back, points on purchase ✓ Need flexibility – Amount may vary ✓ Excellent payment discipline – Won’t carry balance long

Credit Card Advantages

| Advantage | Why It Matters |

|---|---|

| 0% intro offers | True free financing |

| Rewards | Earn cash back on spending |

| Flexibility | Pay any amount above minimum |

| No origination fee | No upfront cost |

| Existing credit | No new application needed |

The Hidden Costs to Consider

Personal Loan Hidden Costs

| Cost | Typical Amount | How to Avoid |

|---|---|---|

| Origination fee | 1-8% of loan | Shop for no-fee lenders |

| Prepayment penalty | Varies | Read terms, ask upfront |

| Late fees | $25-$50 | Set up autopay |

| Application fees | $0-$50 | Most reputable lenders: $0 |

Credit Card Hidden Costs

| Cost | Typical Amount | How to Avoid |

|---|---|---|

| Annual fee | $0-$550 | Use no-annual-fee cards |

| Balance transfer fee | 3-5% | Factor into calculations |

| Cash advance fee | 3-5% + higher APR | Never use cash advances |

| Late fee | $25-$40 | Set up autopay |

| Penalty APR | 29.99% | Never pay late |

| Deferred interest | All interest retroactive | Pay 0% offers in full |

Frequently Asked Questions

Is a personal loan better than a credit card✓

It depends on your situation:

| Scenario | Better Option |

|---|---|

| Large amount ($5,000+) | Personal loan |

| Small amount (<$3,000) | Credit card |

| 0% APR available | Credit card |

| Need fixed payments | Personal loan |

| High credit card rates | Personal loan |

| Want rewards | Credit card |

| Need spending discipline | Personal loan |

Neither is universally better—calculate your specific scenario.

What credit score do I need for a personal loan✓

General guidelines:

| Credit Score | Expected APR | Approval Odds |

|---|---|---|

| 720+ | 6-12% | Excellent |

| 680-719 | 12-18% | Good |

| 640-679 | 18-25% | Fair |

| Below 640 | 25-36% or denied | Poor |

Tip: Check rates without affecting score using prequalification tools.

Does a personal loan hurt your credit✓

Short-term: Small dip (5-10 points) from: – Hard inquiry – New account

Long-term: Can improve credit by: – Adding installment loan diversity – Reducing credit utilization (if consolidating cards) – Building payment history

How much can I borrow with a personal loan✓

Typical ranges:

| Lender Type | Minimum | Maximum |

|---|---|---|

| Online lenders | $1,000 | $50,000 |

| Banks | $2,000 | $100,000 |

| Credit unions | $500 | $50,000 |

Your actual limit depends on income, credit score, and debt-to-income ratio.

What’s the average personal loan interest rate✓

Current averages (2024):

| Credit Score | Average APR |

|---|---|

| Excellent (720+) | 10.3-12.5% |

| Good (690-719) | 13.5-15.5% |

| Fair (630-689) | 17.8-19.9% |

| Poor (300-629) | 28.5-32% |

Compare multiple lenders—rates vary significantly.

Can I use a credit card like a loan✓

Yes, but with cautions:

Approaches: – Balance transfer to 0% card – Large purchase on existing card – New card with introductory offer

Key differences from loan: – Variable rate (can increase) – Minimum payments can extend debt – Temptation to spend more – No fixed end date

Should I consolidate credit card debt with a personal loan✓

Usually yes, if: – Loan rate is significantly lower (5%+ difference) – You won’t rack up new credit card debt – Monthly payment fits your budget – You avoid origination fees or they’re worth it

Be cautious if: – You’ll use freed-up credit – Loan payment strains budget – Rate difference is minimal – You’ve consolidated before and re-accumulated debt

What is an origination fee✓

Definition: Upfront fee charged by lender, typically 1-8% of loan amount.

Example: – Loan amount: $10,000 – Origination fee: 3% – Fee amount: $300 – You receive: $9,700 (or fee added to loan)

Impact: Increases effective APR. A 10% loan with 3% fee is effectively ~11.5% APR.

Are personal loans tax deductible✓

Generally no, with exceptions:

| Use | Deductible✓ |

|---|---|

| Personal expenses | No |

| Home improvement | Possibly (consult tax advisor) |

| Business expenses | Yes (if business loan) |

| Investment | Potentially (investment interest) |

Credit card interest is also not tax deductible for personal use.

How fast can I get a personal loan✓

Typical timelines:

| Lender Type | Application to Funding |

|---|---|

| Online lenders | 1-3 business days |

| Banks | 3-7 business days |

| Credit unions | 2-5 business days |

Fastest options: Some online lenders offer same-day or next-day funding.

What happens if I can’t pay my personal loan✓

Consequences of default:

| Timeline | What Happens |

|---|---|

| 1-29 days late | Late fee, possible rate increase |

| 30+ days late | Reported to credit bureaus |

| 60-90 days | Collections calls, credit damage |

| 90+ days | Charge-off, sent to collections |

| Ongoing | Potential lawsuit, wage garnishment |

If struggling: Contact lender immediately. Many offer hardship programs.

Can I pay off a personal loan early✓

Usually yes, but check for: – Prepayment penalties – Some lenders charge for early payoff – How interest is calculated – Precomputed vs simple interest

Simple interest loans: Pay early, save interest Precomputed interest: May owe all interest regardless

Always ask before signing: “Is there a prepayment penalty✓”

Related Calculators

Make the best financing decision:

- Debt Consolidation Calculator – See full consolidation savings

- Credit Card Payoff Calculator – Plan credit card payoff

- Balance Transfer Calculator – Evaluate 0% offers

- Loan Amortization Calculator – See payment breakdown

This calculator provides estimates for comparison purposes. Actual rates, fees, and terms depend on your credit profile and lender. Always review loan documents carefully before signing.