Interest Rate Reduction Calculator: What Would You Save?

See how much you'd save with a lower interest rate on your debt.

How This Rate Reduction Savings Calculator Works

Our rate reduction savings calculator shows exactly how much you’ll save when you lower your interest rate. See:

- Monthly payment reduction – Your new lower payment

- Total interest saved – Lifetime savings from the lower rate

- Faster payoff – How quickly you’ll be debt-free

- Break-even analysis – When fees pay for themselves

- Comparison scenarios – See 1%, 3%, and 5% reductions

Even a small rate reduction can save thousands of dollars over the life of your loan.

The Math Behind Rate Reductions

Why Rate Matters So Much

Interest rate impacts two things: 1. Monthly payment amount – Higher rate = higher payment 2. Total interest over loan life – Higher rate = more interest paid

The compound effect: Lower rates reduce both monthly cost AND total cost, creating exponential savings on longer loans.

Rate Reduction Formula

Monthly payment calculation:

M = P × [r(1+r)^n] / [(1+r)^n - 1]

Where:

M = Monthly payment

P = Principal (loan amount)

r = Monthly interest rate (APR ÷ 12)

n = Number of paymentsKey insight: Even small rate changes significantly impact the formula’s output.

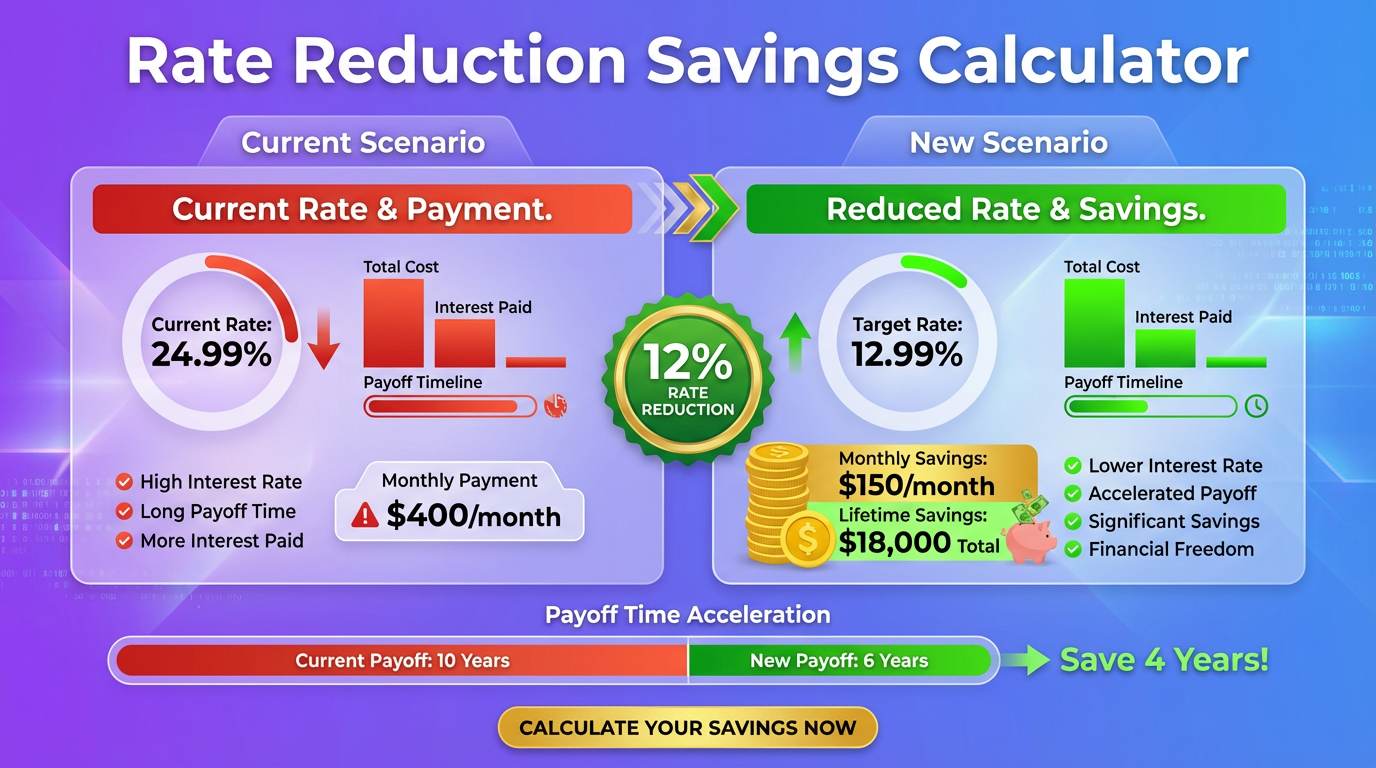

Rate Reduction Examples: Real Savings

Example 1: Credit Card Rate Negotiation ($12,000)

Scenario: Mark calls his credit card company to negotiate a lower rate.

Current Situation: – Balance: $12,000 – Current APR: 24.99% – Monthly payment: $350 – Time to payoff: 50 months – Total interest: $5,364

After Successful Negotiation (19.99% APR):

| Metric | Before (24.99%) | After (19.99%) | Savings |

|---|---|---|---|

| Monthly payment | $350 | $350 | Same |

| Payoff time | 50 months | 45 months | 5 months faster |

| Total interest | $5,364 | $4,013 | $1,351 |

5% rate reduction saves $1,351 with just one phone call.

If rate drops to 14.99%: – Payoff time: 41 months (9 months faster) – Total interest: $2,867 – Total savings: $2,497

Example 2: Auto Loan Refinance ($22,000)

Scenario: Jennifer refinances her car loan after improving her credit score.

Original Loan: – Balance: $22,000 – Original APR: 9.9% – Term: 60 months remaining – Monthly payment: $467 – Total remaining interest: $5,989

Refinanced Loan (5.9% APR):

| Metric | Original (9.9%) | Refinanced (5.9%) | Savings |

|---|---|---|---|

| Monthly payment | $467 | $425 | $42/month |

| Total interest | $5,989 | $3,485 | $2,504 |

4% rate reduction saves: – $42/month × 60 months = $2,520 in payments – $2,504 in interest – Break-even: Immediate (no refinancing fees for auto loans)

Example 3: Mortgage Refinance ($280,000)

Scenario: The Smiths refinance their mortgage when rates drop.

Current Mortgage: – Balance: $280,000 – Current rate: 7.25% – Remaining term: 27 years (324 months) – Monthly payment: $1,966 – Remaining interest: $356,584

Refinanced Mortgage (6.25%):

| Metric | Original (7.25%) | Refinanced (6.25%) | Savings |

|---|---|---|---|

| Monthly payment | $1,966 | $1,797 | $169/month |

| Total interest | $356,584 | $302,068 | $54,516 |

Refinancing Costs: $6,500 (closing costs)

Net Savings: $54,516 – $6,500 = $48,016

Break-even: $6,500 ÷ $169 = 38 months (3.2 years)

If they stay 10+ years: Refinancing is clearly worth it.

Example 4: Student Loan Refinance ($45,000)

Scenario: David refinances federal loans to a private lender for lower rate.

Current Loans: – Balance: $45,000 – Weighted average rate: 6.8% – Remaining term: 8 years – Monthly payment: $608 – Remaining interest: $13,368

After Refinancing (4.5% APR):

| Metric | Federal (6.8%) | Refinanced (4.5%) | Savings |

|---|---|---|---|

| Monthly payment | $608 | $567 | $41/month |

| Total interest | $13,368 | $8,432 | $4,936 |

2.3% rate reduction saves $4,936.

⚠ Important Trade-off: David loses federal protections: – Income-driven repayment options – PSLF eligibility – Federal forbearance/deferment

Best for: Private sector workers with stable income who won’t qualify for forgiveness.

Example 5: Personal Loan Consolidation ($18,000)

Scenario: Lisa consolidates credit cards into a personal loan.

Current Credit Cards: | Card | Balance | APR | Min Payment | |——|———|—–|————-| | Card A | $8,000 | 26.99% | $200 | | Card B | $6,000 | 22.99% | $150 | | Card C | $4,000 | 19.99% | $100 | | Total | $18,000 | 24.3% avg | $450 |

If paid at $450/month: – Payoff time: 62 months – Total interest: $10,032

Personal Loan at 11.99% APR:

| Metric | Credit Cards | Personal Loan | Savings |

|---|---|---|---|

| APR | 24.3% avg | 11.99% | -12.3% |

| Monthly payment | $450 | $400 | $50/month |

| Payoff time | 62 months | 54 months | 8 months faster |

| Total interest | $10,032 | $3,629 | $6,403 |

12% rate reduction saves $6,403 and eliminates debt 8 months sooner.

Rate Reduction Savings by Loan Type

Quick Reference Tables

Credit Cards (Per $10,000 balance, $300/month payment):

| Rate Change | Months Saved | Interest Saved |

|---|---|---|

| 25% → 20% | 3 months | $912 |

| 25% → 15% | 7 months | $1,824 |

| 25% → 10% | 10 months | $2,564 |

| 25% → 0% | 14 months | $3,416 |

Auto Loans (Per $25,000, 60-month term):

| Rate Change | Monthly Savings | Total Savings |

|---|---|---|

| 10% → 8% | $23 | $1,380 |

| 10% → 6% | $47 | $2,820 |

| 10% → 4% | $71 | $4,260 |

Mortgages (Per $300,000, 30-year term):

| Rate Change | Monthly Savings | Total Savings |

|---|---|---|

| 7% → 6.5% | $100 | $36,000 |

| 7% → 6% | $199 | $71,640 |

| 7% → 5.5% | $298 | $107,280 |

| 7% → 5% | $396 | $142,560 |

How to Get a Lower Rate

Strategy 1: Call and Ask (Credit Cards)

Success rate: 60-70% for cardholders in good standing

Script: > “Hi, I’ve been a customer for [X years] and have always paid on time. I’ve received offers from other cards at lower rates. Can you reduce my APR to help me stay with [card name]✓”

Tips: – Have competing offers ready – Mention your payment history – Ask for a supervisor if first rep says no – Call during business hours (decision-makers available)

Strategy 2: Refinance (Auto/Mortgage/Student)

When refinancing makes sense: – Rate dropped 0.5-1%+ since original loan – Credit score improved significantly – Can afford closing costs (mortgage) – Will stay in home/keep car long enough

Where to check rates: – Credit unions (often lowest rates) – Online lenders – Local banks – Mortgage brokers (for home loans)

Strategy 3: Consolidate (Multiple Debts)

Good candidates for consolidation: – Multiple credit cards at high rates – Good enough credit for personal loan (680+) – Committed to not running cards back up – Total debt under $50,000

Strategy 4: Balance Transfer

Temporary rate reduction: – 0% APR for 12-21 months – Transfer fee: 3-5% – Must pay off before promo ends

Best for: Debts you can pay off within promo period.

Break-Even Analysis

When Do Fees Pay for Themselves✓

Formula:

Break-Even (months) = Total Fees ÷ Monthly SavingsExamples:

| Scenario | Fees | Monthly Savings | Break-Even |

|---|---|---|---|

| Credit card negotiation | $0 | $35 | Immediate |

| Auto refinance | $0 | $42 | Immediate |

| Balance transfer | $450 | $200 | 2.3 months |

| Mortgage refinance | $6,500 | $169 | 38 months |

| Student loan refinance | $0 | $41 | Immediate |

Should You Refinance✓

Yes, if: – Break-even is less than time you’ll keep the loan – You won’t incur prepayment penalties – Benefits outweigh lost protections (student loans) – You can qualify for meaningfully lower rate

No, if: – Break-even exceeds remaining loan term – High prepayment penalties – Need federal loan protections – Credit score won’t qualify for better rate – Planning to sell home soon (mortgage)

Rate Reduction by Credit Score

What Rate Can You Get✓

Credit Cards: | Credit Score | Typical APR Range | |————–|——————-| | 750+ | 12-18% | | 700-749 | 18-22% | | 650-699 | 22-26% | | Below 650 | 26-30%+ |

Auto Loans: | Credit Score | New Car APR | Used Car APR | |————–|————-|————–| | 750+ | 4-6% | 5-7% | | 700-749 | 6-8% | 7-10% | | 650-699 | 8-12% | 10-14% | | Below 650 | 12-18% | 14-20%+ |

Mortgages: | Credit Score | Typical Rate Impact | |————–|———————| | 760+ | Best available rate | | 700-759 | +0.25-0.5% | | 680-699 | +0.5-1% | | 620-679 | +1-2% | | Below 620 | May not qualify |

Improving your score by 50-100 points can save thousands in interest.

Frequently Asked Questions

How much can I save with a lower interest rate✓

Savings depend on: – Current rate vs. new rate (bigger gap = more savings) – Loan balance (higher balance = more savings) – Remaining term (longer term = more savings)

Rule of thumb: On a $200,000 mortgage, each 0.5% rate reduction saves ~$60/month and ~$20,000 over 30 years.

Is a 1% rate reduction worth it✓

Usually yes, especially for large balances:

| Loan Type | Balance | 1% Saves (Total) |

|---|---|---|

| Credit card | $10,000 | $500-$1,500 |

| Auto loan | $25,000 | $700-$1,500 |

| Mortgage | $300,000 | $35,000-$40,000 |

For mortgages, even 0.5% is often worthwhile.

How do I negotiate a lower credit card rate✓

Steps: 1. Know your current rate and payment history 2. Research competing offers 3. Call customer service 4. State you want a rate reduction 5. Mention your loyalty and payment history 6. Reference competing offers 7. Ask for supervisor if initial answer is no 8. Be polite but persistent

Success rate: 60-80% for customers with good payment history.

Will refinancing hurt my credit score✓

Short-term: Yes, slightly – Hard inquiry: -5 to -10 points – New account: -5 to -10 points – Average account age decreases

Long-term: Often neutral or positive – Lower utilization (if consolidating cards) – On-time payments on new loan – Paying off old accounts

Impact fades within 6-12 months and long-term benefits outweigh short-term hit.

How often can I refinance✓

No hard rules, but consider:

| Loan Type | Practical Frequency |

|---|---|

| Auto | Anytime if rate improves significantly |

| Mortgage | Every 2-3 years if rates drop 0.5%+ |

| Student | Usually once (federal → private) |

| Personal | When credit improves significantly |

Watch for: Prepayment penalties, closing costs, application fees.

What’s better: lower rate or shorter term✓

Compare both scenarios:

| $200,000 Mortgage | Lower Rate | Shorter Term |

|---|---|---|

| Original | 7%, 30 yr, $1,331/mo | 7%, 30 yr, $1,331/mo |

| Option | 6%, 30 yr, $1,199/mo | 7%, 15 yr, $1,798/mo |

| Monthly change | -$132 | +$467 |

| Total interest | $231,640 | $123,640 |

| Savings | $106,280 | $214,280 |

Shorter term saves more but requires higher payments. Choose based on budget and goals.

Should I pay points to lower my rate✓

Points = prepaid interest (1 point = 1% of loan amount)

Break-even calculation:

Point Cost ÷ Monthly Savings = Break-Even MonthsExample: $300,000 mortgage – 1 point costs: $3,000 – Rate reduction: 0.25% – Monthly savings: $50 – Break-even: 60 months (5 years)

Pay points if: Staying 5+ years and have cash available

What fees should I watch for when refinancing✓

Common fees:

| Fee Type | Typical Cost | Who Charges |

|---|---|---|

| Origination | 0.5-1% of loan | Lender |

| Appraisal | $300-$600 | Third party |

| Title search | $200-$400 | Title company |

| Closing costs | 2-5% of loan | Various |

| Prepayment penalty | 1-3% of balance | Original lender |

Always calculate total fees vs. total savings.

Can I get a lower rate with bad credit✓

Options for lower-than-current rates: – Secured credit cards (lower rates, require deposit) – Credit union loans (often more flexible) – Co-signed loans (use someone’s better credit) – Credit-builder loans (establish history) – Wait and improve credit first

Improving credit score is often the best path to meaningfully lower rates.

How long does refinancing take✓

Typical timelines:

| Loan Type | Processing Time |

|---|---|

| Auto refinance | 1-3 days |

| Personal loan | 1-7 days |

| Student loan refinance | 2-4 weeks |

| Mortgage refinance | 30-45 days |

Auto and personal loans are fastest; mortgages require appraisals and title work.

Does rate reduction affect my loan term✓

Depends on your choice:

Option A: Keep same payment → Shorter term, more interest saved Option B: Lower payment → Same term, lower monthly cost

Example: Refinance from 7% to 6% – Keep payment: Pay off 4 years early, save more interest – Lower payment: Enjoy $150/month savings, same payoff date

Most experts recommend keeping payments the same to maximize savings.

What if my rate request is denied✓

Next steps: 1. Ask why (helps you improve) 2. Request reconsideration with supervisor 3. Try again in 6 months 4. Improve factors they mentioned 5. Try different lender 6. Consider balance transfer offers 7. Focus on paying down balance (lower utilization)

Don’t give up – persistence and improved credit often succeed.

Related Calculators

Maximize your rate reduction strategy:

- Refinancing Calculator – Full refinance analysis

- Balance Transfer Calculator – Evaluate 0% offers

- Debt Consolidation Calculator – Combine debts at lower rate

- True Interest Cost Calculator – See current interest drain

This calculator provides estimates based on the rates you enter. Actual rates depend on creditworthiness, lender policies, and market conditions. Always compare multiple offers before refinancing.