If you’re struggling with multiple high-interest credit cards, debt consolidation can feel like both a financial and emotional lifeline. But if you’ve never consolidated debt before, the process can feel confusing or intimidating.

“How does it work?”

“What happens when I call?”

“Will I understand it?”

“Do I need good credit?”

Those are exactly the questions first-time borrowers ask, and the ones many people end up answering for themselves once they’ve walked through the process with Lendwyse.

Below is a detailed walkthrough of how the debt consolidation process works for first-time borrowers at Lendwyse, enriched with real experiences from Trustpilot reviewers who have been where you are now.

Table Of Contents:

- What is Debt Consolidation Really?

- Step 1: The First Conversation: Setting the Foundation

- Step 2: Reviewing Your Financial Picture

- Step 3: Exploring Your Options Clearly and Without Jargon

- Step 4: The Decision Stage: No Pressure, Just Information

- Step 5: Enrollment, If and When You’re Ready

- What Happens After Enrollment: Your Consolidation Plan in Action

- First-Time Borrower Stories: Real Voices, Real Experiences

- Common Questions First-Time Borrowers Ask

- What First-Timers Often Get Wrong Before They Start

- What Happens When You Succeed with Consolidation

- Final Takeaways for First-Time Borrowers

- Ready to Explore Your Options?

What is Debt Consolidation Really?

Before we get into what happens step-by-step, it helps to be clear on what debt consolidation actually means.

Debt consolidation is a strategy where you combine multiple debts — like credit cards, store cards, or other unsecured balances — into a single obligation. The idea is to simplify your payments and ideally lower your overall interest or monthly payment so you can pay down debt faster and more predictably.

For a first-time borrower, this can feel like a big shift from juggling multiple bills to having one plan that’s easier to manage. It’s not just about getting one payment but about creating structure and clarity around what you owe.

At Lendwyse, the goal is to help you understand whether consolidation is a realistic fit for your specific situation, not to push you into a one-size-fits-all approach.

Step 1: The First Conversation: Setting the Foundation

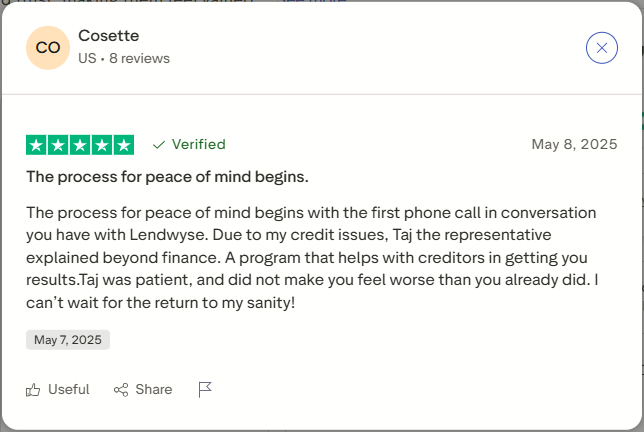

The consolidation process usually begins with a simple consultation call, and here’s where many people’s fears evaporate.

One reviewer captured the feeling of that first discussion perfectly:

“The process for peace of mind begins with the first phone call in conversation you have with Lendwyse.”

This initial call isn’t a sales pitch but an opportunity for a trained specialist to understand your financial picture and begin mapping out whether consolidation makes sense for you.

Expect the specialist to ask questions like:

-

How many credit cards or debts do you have?

-

What are your interest rates?

-

What are your current monthly payments?

-

How long have you been managing these debts?

-

What are you hoping to achieve?

One Trustpilot reviewer noted how much comfort came from this stage:

“Almas made my experience great. He listened to me and tailored the program to my needs…”

That personalization is key. Debt isn’t a one-size-fits-all problem, and your consultation should reflect that.

Step 2: Reviewing Your Financial Picture

Once the initial rapport is established, your specialist will look at the numbers — not to judge you, but to understand what you’re working with.

This part of the process focuses on:

-

Current balances on all unsecured debts (e.g., credit cards)

-

Interest rates and whether they are variable

-

Monthly payments and due dates

-

Whether accounts are current or in arrears

-

Your income and ability to make payments

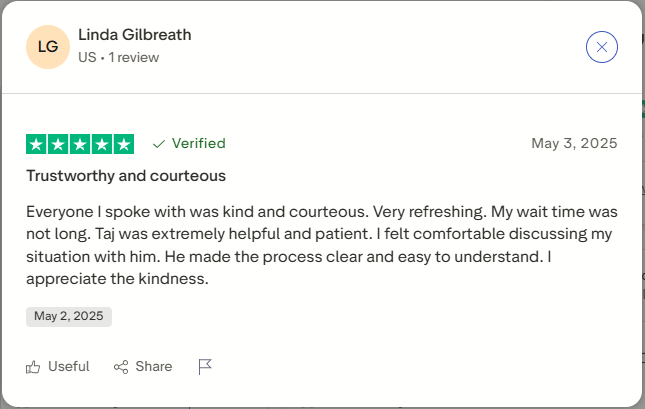

Many reviewers highlight how respectful and informative this stage feels:

“Everyone I spoke with was kind and courteous… I felt comfortable discussing my situation with him.”

That’s crucial, because a clear financial snapshot is the foundation of any good consolidation plan. It also helps your specialist determine whether debt consolidation is appropriate or whether other options might fit better.

Step 3: Exploring Your Options Clearly and Without Jargon

After understanding your financial picture, your specialist will walk you through what your options look like — in plain language.

This is where the concept of debt consolidation becomes real.

Instead of talking about “interest rates” and “amortization schedules,” most first-time borrowers remember being walked through things like:

-

“If we combine these five accounts, here’s how your total monthly payment could change.”

-

“Here’s how much interest you’re paying now versus what you could pay with consolidation.”

-

“This helps you focus on one payment so you’re not juggling multiple due dates.”

One reviewer who initially didn’t understand the options was pleasantly surprised:

“Kameel was very helpful… he explained everything and made it clear… I felt like a valued customer…”

And another emphasized how patience and explanation made all the difference:

“Michael Hamilton… listened to me and tailored the program to my needs, which was very much appreciated.”

This clarity helps first-time borrowers shift from feeling overwhelmed to feeling in control of their debt strategy.

Step 4: The Decision Stage: No Pressure, Just Information

Many people entering debt consolidation for the first time fear that they’ll be pressured into making a quick decision. But according to real reviewers, that’s not how it works at LendWyse.

Instead, you’re given:

-

Clear explanations

-

Realistic expectations

-

Room to think things through

-

A chance to ask as many questions as you need

One reviewer described how the process felt calm and respectful:

“The experience was calm. I never felt pressured.”

This lack of pressure is intentional. Decision confidence comes from understanding, not urgency.

Step 5: Enrollment, If and When You’re Ready

If you decide that consolidation aligns with your goals and financial situation, the next step is enrollment.

This usually involves:

-

Agreeing to a consolidation plan

-

Signing paperwork (often electronically)

-

Setting up your payment schedule

-

Receiving guidance on next steps

One reviewer who chose to move forward said:

“Emily Pitman… worked with me thoroughly — the process of signing up was simple and efficient.”

For first-timers, this can feel empowering because it marks a clear transition from confusion and stress to action.

What Happens After Enrollment: Your Consolidation Plan in Action

Once you’re enrolled in a debt consolidation plan, here’s what typically happens:

1. One Monthly Payment

Instead of juggling multiple cards and due dates, you’ll have one payment to focus on each month, which can reduce stress and improve consistency.

2. A Structured Timeline

Consolidation plans usually come with a clear timeline, so you can see when your debt could be paid off. This is hard to visualize when you’re dealing with multiple accounts.

3. Potentially Lower Interest

Depending on your plan, consolidation can reduce the total interest you pay over time, letting more of your money go toward principal.

4. Ongoing Communication

Many clients appreciate that their specialist remains available to answer questions or address concerns as the plan progresses.

First-Time Borrower Stories: Real Voices, Real Experiences

One of the most powerful ways to understand how debt consolidation works at Lendwyse is to hear from first-time borrowers themselves. Here are some representative experiences from Trustpilot reviewers who were once in your shoes:

Feeling Understood and Not Judged

“I wasn’t made to feel like I was an awful person, very understanding and personable.”

This sentiment repeats across dozens of reviews. People appreciate being treated with empathy rather than condemnation.

Clarity Matters More Than Anything

“Zachery was great at explaining everything and very knowledgeable and friendly…”

Understanding how consolidation fits your life makes a huge difference.

Patience with Questions

“Kevin was amazing answered all my dumb questions… after everything was explained the instant relief… made a lighter load.”

That review reflects a common theme: learn first, commit later. There’s no such thing as a bad question.

Guiding You Through Every Step

“My Consolidation Specialist, Alen Baits… was outstanding in taking the time to walk me thru every step.”

For first-timers, that guidance turns fear into clarity.

Finding Hope Where There Was None

“I can’t even thank you enough for taking care of my debt… I should’ve done this a long time ago. I’m so happy…”

This kind of up-front enthusiasm often comes after folks finally understand their options.

Common Questions First-Time Borrowers Ask

Here are some questions newcomers often have, answered in plain language:

Q: Do I need good credit to qualify for consolidation?

Not necessarily. A debt consolidation plan often focuses on your overall ability to manage and repay your debts, not just a single credit score number.

Q: How long does the process take?

The initial consultation is usually one call. Enrollment (if you choose to proceed) can often happen immediately or within a short time thereafter.

Q: Is consolidation right for everyone?

Not always, but the consultation will help you determine whether it’s a fit for your situation.

What First-Timers Often Get Wrong Before They Start

Before people go through the process, they tend to make assumptions like:

“I’m too far in debt.”

“I’ll be judged.”

“It’ll ruin my credit more.”

“It’s too complicated.”

But first-hand reviews show important truths:

- You can explore options even if debt feels overwhelming.

- You won’t be judged for your financial past.

- You will learn whether a strategy is right for you.

What Happens When You Succeed with Consolidation

Debt consolidation isn’t just a technical financial tool. It’s a transition from stress to stability. Many first-timers report not just financial gains, but emotional relief:

“I was hesitant at first but he explained everything… I felt like a valued customer.”

That sense of being valued and understood is a recurring theme in LendWyse reviews, and for many, it’s the true value of the process.

Final Takeaways for First-Time Borrowers

Here’s what you should keep in mind if you’re considering debt consolidation at Lendwyse:

It Starts with Understanding

The first conversation isn’t a commitment. It’s clarity.

It’s Personal, Not Generic

You’re not just another number. Specialists take time to understand your situation.

Questions Are Encouraged

There’s no such thing as a bad question, especially when it helps you understand your plan better.

You Decide When You’re Ready

No pressure. Just information.

Many People Wish They Had Called Sooner

Real reviewers often reflect that starting consolidation earlier would have saved them time and stress.

Ready to Explore Your Options?

If you’re tired of juggling multiple interest-laden payments and want a clearer path to paying off your debt, debt consolidation might be right for you.

And it all starts with a simple conversation.

👉 Talk to Lendwyse today to see how debt consolidation could work for you.