There’s a moment when you shift from thinking “I should be able to handle this debt myself” to realizing “I need to get help.”

It’s not a weakness.

It’s not failure.

It’s clarity.

Real LendWyse customers describe the signs that told them it was time: the sleepless nights that became unbearable, the calculations that never added up, the stress that started affecting everything else in life.

Let’s explore the specific signals that indicate you’re ready.

Table Of Contents:

- #1: You’ve Been “Handling It” for Over a Year Without Progress

- #2: You’re Losing Sleep Over Your Finances

- #3: You Can’t Answer “When Will I Be Debt-Free?”

- #4: The Interest Is Eating Your Payments

- #5: You’re Avoiding Looking at Your Accounts

- #6: Shame Is Keeping You Isolated

- #7: Your Relationships Are Suffering

- #8: You’ve Tried Multiple DIY Solutions

- #9: The Stress Is Affecting Your Health

- #10: You’re Making Decisions Based on Debt, Not Goals

- #11: You’re Getting More Behind Despite Trying Harder

- #12: You’re Feeling Hopeless About Your Financial Future

- #13: You’re Considering Desperate Measures

- #14: You’ve Realized Pride Is Expensive

- #15: You’re Experiencing the “3 AM Clarity”

- The Readiness Checklist: How Many Signs Do You Recognize?

- The Cost of Waiting

- The Bottom Line: Trust Your Gut

#1: You’ve Been “Handling It” for Over a Year Without Progress

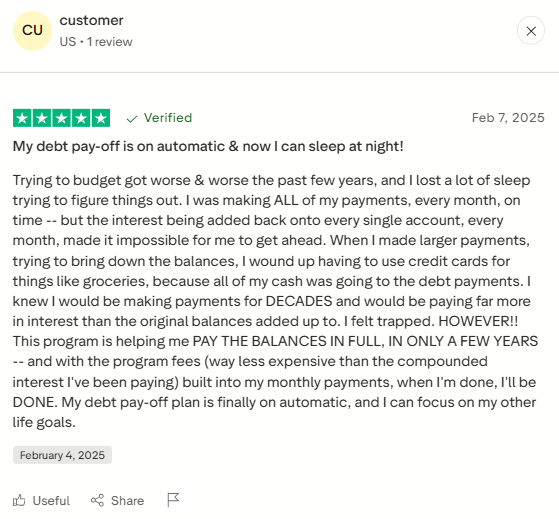

One LendWyse customer captured this perfectly: “Trying to budget got worse & worse the past few years, and I lost a lot of sleep trying to figure things out. I was making ALL of my payments, every month, on time—but the interest being added back each month was keeping me in a never-ending cycle.”

Notice: “past few years.” This wasn’t a recent problem. It was an extended struggle.

The “handling it” trap:

- Making all minimum payments faithfully

- Never missing due dates

- Sticking to your budget

- Doing everything “right”

- But the balance is barely moving after months or years

You recognize that effort without results isn’t noble. It’s unsustainable. You’ve given the DIY approach a fair chance. Time to try something different.

Tamaira Barnes-Hart expressed what many feel: “I should have done this along time ago.”

That regret about waiting reveals the sign: if you’ve been struggling for 12+ months without meaningful progress, you’re ready for help. The only question is whether you’ll acknowledge it.

#2: You’re Losing Sleep Over Your Finances

The same customer mentioned they “lost a lot of sleep trying to figure things out.”

Occasional financial worry is normal. Chronic sleep disruption is a clear signal.

Occasional worry:

- Think about finances before sleep

- Occasional restless night

- Can still function normally

Ready-for-help signal:

- Regularly wake at 3 AM with racing thoughts

- Mind constantly calculating payments

- Exhausted but can’t shut brain off

- Sleep deprivation affects everything else

Mother of the groom described: “Stress is horrible and after everything was explained the instant relief and looking forward to a resolution has made a lighter load.”

The fact that stress was “horrible” suggests the sleep disruption had reached crisis levels. When you can’t remember the last good night’s sleep because of financial anxiety, you’re ready.

#3: You Can’t Answer “When Will I Be Debt-Free?”

Jorge’s experience reveals what changes with help: “Speaking to Kevin today felt like a great relief to taking the next step into setting me up in a plan to reduce and finalize my accumulated dept. I can’t wait for these next 3 years to go by and be debt free!”

Before you’re ready:

- “Hopefully in a few years?”

- “Eventually?”

- “I don’t really know…”

- Can’t calculate the actual timeline

- Hope things will somehow work out

You realize “eventually” and “hopefully” aren’t plans. They’re wishes.

You want a concrete answer: “In exactly X months, I’ll be debt-free.”

The desire for that specific timeline indicates readiness for professional help.

#4: The Interest Is Eating Your Payments

The customer described: “the interest being added back each month was keeping me in a never-ending cycle.”

Treadmill indicators:

- Pay $500, balance drops $200 (after interest)

- Calculate: paying mostly interest, minimal principal

- Feel like running in place

- Motivation erodes when there is minimal progress

- Frustration grows despite consistent effort

You’ve done the math and realized that at the current pace, you’re looking at 15-20 years to pay off. You’re paying double or triple your original debt in total interest. The numbers make you physically sick.

That sick feeling is readiness. You’re no longer willing to donate tens of thousands to credit card companies just because you “should” handle it alone.

#5: You’re Avoiding Looking at Your Accounts

When checking your bank balance triggers anxiety so severe you simply stop checking, you’re ready.

Avoidance behaviors:

- Haven’t logged into accounts in weeks

- Delete bank emails without reading

- Throw away credit card statements unopened

- Don’t answer calls from unknown numbers

- Panic when forced to check the balance

You recognize avoidance isn’t protecting you. It’s making things worse. You want to face reality but need support to do it.

Linda Gilbreath’s experience shows what changes: “I felt comfortable discussing my situation with him.”

That comfort “discussing my situation” only comes after acknowledging you have a situation that needs discussing.

#6: Shame Is Keeping You Isolated

Amy Barnard’s relief was telling: “I wasn’t made to feel like I was an awful person, very understanding and personable.”

The fact that she needed that reassurance reveals how much shame she’d been carrying.

Isolation indicators:

- Haven’t told anyone about debt extent

- Avoid social situations involving money

- Make excuses to decline invitations

- Feel constantly judged (real or imagined)

- Believe you’re uniquely irresponsible

- Carry the burden completely alone

One customer expressed: “Everyone I spoke with were very understanding, helpful and treated me with such respect. We all encounter some sort of hardship and don’t want to be judged for decisions that were made.”

Readiness means recognizing that isolation isn’t protecting your dignity but amplifying your suffering. You’re ready to risk being seen in order to get help.

#7: Your Relationships Are Suffering

Multiple reviews mention discussing debt with spouses or partners, suggesting a household-wide impact.

Relationship strain signs:

- Frequent money arguments

- Avoiding financial discussions

- Tension you can’t name but feel constantly

- Different spending philosophies cause conflict

- Intimacy suffers under stress

- Can’t make joint plans due to uncertainty

You realize debt isn’t just your problem. It’s affecting everyone you love. The desire to protect your relationships becomes stronger than pride about “handling it yourself.”

When you start thinking, “This is hurting my family, not just me,” you’re ready.

#8: You’ve Tried Multiple DIY Solutions

David North’s journey: “Well, I was a little skeptical at first, but he made a lot of sense in what he was saying as far as me trying to pay two cards off and going with beyond…”

DIY attempts often include:

- Balance transfer cards (temporary relief, then same problem)

- Debt snowball method (not working fast enough)

- Strict budgeting (maxed out, nowhere left to cut)

- Extra income attempts (burnout from overwork)

- Negotiating with creditors yourself (limited success)

You’ve exhausted reasonable self-help options and it’s not sufficient for your situation.

Tamaira Barnes-Hart’s “I should of done this along time ago” suggests she’d tried other approaches first. Readiness comes when you’ve proven to yourself that you need more than DIY can provide.

#9: The Stress Is Affecting Your Health

Financial stress doesn’t stay mental. It becomes physical.

Physical stress signs:

- Chronic headaches

- Stomach problems

- High blood pressure

- Chest tightness

- Muscle tension

- Exhaustion despite adequate sleep

- Getting sick more frequently

When health issues (whether pre-existing or stress-induced) are compounded by financial anxiety, you recognize that getting help isn’t optional. It’s necessary for your well-being.

#10: You’re Making Decisions Based on Debt, Not Goals

Jorge’s relief shows what changes: “I can’t wait for these next 3 years to go by and be debt-free!”

He can now envision life beyond debt. Before help, debt controlled all decisions.

Debt-controlled decisions:

- Can’t change jobs (need income stability)

- Can’t move cities (too financially unstable)

- Can’t start family (not financially ready)

- Can’t pursue education (all money to debt)

- Can’t take opportunities (everything filtered through debt lens)

You realize you’re not living your life; you’re living in service to debt. The desire to reclaim agency over your decisions indicates readiness.

When you catch yourself thinking “I can’t do X because of debt” for the hundredth time and feel rage instead of resignation, that’s readiness.

#11: You’re Getting More Behind Despite Trying Harder

One customer noted: “Trying to budget got worse & worse the past few years.”

Despite trying, things deteriorated. This isn’t your fault. It’s math working against you.

The backwards slide:

- Cut expenses to the bone

- Work extra hours

- Apply every dollar to debt

- Yet balance increases or stays stagnant

- Interest compounds faster than you can pay

- Unexpected expenses derail progress

You recognize that individual willpower can’t overcome the mathematical reality of a 22% compound interest. You’re not weak; you’re facing structural problems that require structural solutions.

#12: You’re Feeling Hopeless About Your Financial Future

The customer trapped in a “never-ending cycle” captures the hopelessness that indicates readiness.

Hopelessness indicators:

- Can’t imagine being debt-free

- Feel trapped indefinitely

- Lost motivation to try

- Going through motions without belief

- Think “This will never end”

- Depression about your financial situation

Paradoxically, recognizing hopelessness is readiness. You’re acknowledging the current approach isn’t working. You’re open to something different because you can’t continue this way.

#13: You’re Considering Desperate Measures

Desperation indicators:

- Considering payday loans

- Thinking about 401(k) loans or withdrawals

- Contemplating borrowing from family

- Looking at home equity despite risks

- Researching bankruptcy prematurely

- Considering lying on loan applications

When you catch yourself considering options that feel wrong, dangerous, or desperate, that’s your internal warning system saying, “Get proper help before you make this worse.”

JANET RANK’s experience shows healthy redirection: “Maurice was so helpful and kind. I did not qualify for a personal loan and he helped me understand what alleviate could do to help me.”

Rather than desperate measures, she found appropriate solutions through professional guidance. Readiness means seeking expert advice before desperation drives poor decisions.

#14: You’ve Realized Pride Is Expensive

Tamaira Barnes-Hart: “I should of done this along time ago.”

That regret about waiting reveals the expensive lesson: pride costs money.

Pride’s price tag:

- Years of unnecessary interest paid

- Thousands in excess charges

- Stress affects health, relationships, and work

- Opportunities missed while in survival mode

- Time that can’t be recovered

You calculate what pride has cost you so far and what it will cost if you wait another year. The financial and personal price of “handling it yourself” exceeds any ego benefit.

When you’d rather save $10,000 and your sanity than prove you don’t need help, you’re ready.

#15: You’re Experiencing the “3 AM Clarity”

Many clients describe a specific moment when everything crystallized.

The 3 AM realization:

- Can’t sleep (again)

- Mind racing (again)

- Calculating (again)

- Suddenly think: “I can’t keep doing this.”

- Crystal clarity that something must change

- Morning resolve to seek help

The Readiness Checklist: How Many Signs Do You Recognize?

You’re likely ready for help if you:

□ Have struggled with debt for 12+ months without progress

□ Regularly lose sleep over finances

□ Can’t answer “When will I be debt-free?”

□ Watch interest eat most of your payments

□ Avoid looking at account balances

□ Feel ashamed and isolated about debt

□ Notice relationship strain from financial stress

□ Have tried multiple DIY solutions that didn’t work

□ Experience physical health impacts from stress

□ Make all major decisions based on debt

□ Work harder but fall further behind

□ Feel hopeless about your financial future

□ Consider desperate measures

□ Realize pride is costing you money □ Have had the “3 AM clarity” moment

If you checked 3+ signs: You’re ready

If you checked 5+ signs: You’re overdue

If you checked 8+ signs: Getting help is urgent

The Cost of Waiting

What waiting costs:

Every month of delay at 22% APR on $15,000:

- Interest charges: ~$275

- Stress continuing: Immeasurable

- Sleep lost: Countless hours

- Opportunities missed: Unknown but real

What acknowledging readiness provides:

- Interest savings starting immediately

- Stress relief from having a plan

- Sleep returning

- Life resuming

The best time to get help was when you first noticed these signs. The second-best time is now.

The Bottom Line: Trust Your Gut

Deep down, you know whether you’re ready. The signs aren’t subtle — they’re your mind, body, and life screaming for change.

As a customer expressed: “We all encounter some sort of hardship and don’t want to be judged for decisions that were made.”

Acknowledging readiness isn’t admitting failure. It’s demonstrating wisdom and recognizing when professional help serves you better than continued solo struggle.

The question isn’t “Am I ready?” You already know the answer.

The question is: “Will I acknowledge what I know and act on it?”

Ready to Take the Next Step?

If you recognized yourself in three or more of these signs, you’re ready for help, whether you’ve fully acknowledged it yet or not.

What clients discovered when they acknowledged they need help with debt:

- Instant relief from finally seeking help

- Clear path replacing endless confusion

- Support replacing isolation

- Hope replacing despair

- Progress replacing stagnation

Stop waiting for things to get worse before you acknowledge you’re ready. Stop hoping you’ll suddenly develop superhuman financial powers.

You’re ready when you recognize you’re ready. These signs are your internal guidance system saying: “It’s time.”