In hundreds of verified LendWyse reviews, a recurring theme emerges:

“I should have done this sooner.”

But embedded in these testimonials are deeper revelations. Things customers wish they’d understood before starting their debt consolidation journey.

These aren’t complaints; they’re hard-won insights that could help others avoid unnecessary stress, make better decisions, and set appropriate expectations.

By analyzing what real customers say they learned through experience, we can provide the knowledge they wish they’d had from day one.

Let’s explore the wisdom that comes from 600+ verified experiences, distilling the insights that matter most for anyone considering debt consolidation.

Table Of Contents:

- 1. Understanding Takes Time

- 2. Your Credit Score Isn’t Your Only Value

- 3. “Instant” Doesn’t Mean Easy

- 4. Questions Aren’t Burdens

- 5. Not Qualifying for Loans Doesn’t Mean No Options

- 6. Realistic Timelines Beat Optimistic Fantasies

- 7. The Hardest Part Is Starting, Not Continuing

- 8. Follow-Up Support Matters More Than Initial Setup

- 9. Your Situation Isn’t as Unique as You Think

- 10. Spending Discipline Is Non-Negotiable

- 11. Patience and Kindness Are Essentials

- 12. Accommodations Are Available, You Just Have to Ask

- 13. The Total Cost Matters More Than The Monthly Payment

- 14. Your Emotional State Will Affect Your Decision

- 15. Success Requires Active Participation, Not Passive Hope

- The Bottom Line: Learn Before, Not During

1. Understanding Takes Time

Kate reflected: “Alen Baits was so incredibly helpful and thorough with everything we discussed! This process, which I was dreading, was extremely easy and stress-free because of him. I didn’t have to ask many questions because he explained everything so well.”

Many people approach debt consolidation feeling that they should already understand financial concepts. They’re embarrassed to ask “basic” questions and rush through explanations, pretending to understand.

Understanding complex financial programs takes time. Good specialists expect this and build time into the process. There’s no shame in needing thorough explanations. In fact, asking questions demonstrates intelligence, not ignorance.

Don’t pretend to understand when you don’t. Don’t rush through explanations to appear smart. Good debt relief specialists welcome questions.

MARILYNZAMUDIO expressed: “Mr Almas Alebikov is excellent with what he does. He ‘walked’ me through everything and made me feel comfortable despite my limited knowledge and experience in dealing with financial issues.”

Thorough understanding is your right, not an imposition. Specialists who rush you aren’t doing their job. Take the time you need.

2. Your Credit Score Isn’t Your Only Value

Kameel’s customer noted: “Kameel was very understanding he didn’t make me feel like I was an irresponsible person. He was very thorough in explaining how the process works and what to expect.”

Many people believe bad credit = bad person. They approach debt consolidation expecting judgment and assuming their low credit score disqualifies them from help or respect.

Credit scores reflect past circumstances, not character. Many legitimate reasons exist for damaged credit: medical emergencies, job loss, divorce, or lack of financial education. Progressive debt relief companies evaluate complete situations, not just three-digit numbers.

Your credit score is one data point among many. Your income stability, employment history, commitment to change, and complete circumstances all matter. Don’t assume low credit means no options or no respect.

3. “Instant” Doesn’t Mean Easy

Mother of the groom described: “Stress is horrible and after everything was explained the instant relief and looking forward to a resolution has made a lighter load.”

Many people think relief only comes after debt is eliminated. They steel themselves for years of continued suffering until the final payment.

The benefit isn’t just eventual debt freedom. It’s immediate peace of mind from understanding your situation, having a clear plan, and no longer facing it alone. The journey itself should feel better, not just the destination.

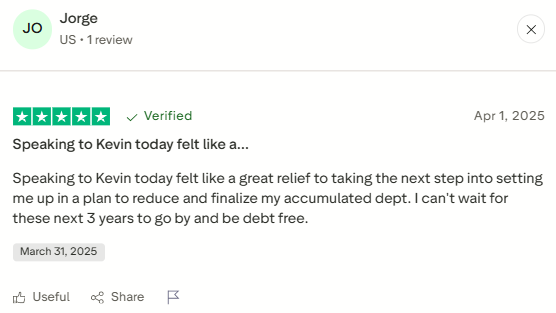

Jorge experienced: “Speaking to Kevin today felt like a great relief to taking the next step into setting me up in a plan to reduce and finalize my accumulated dept.”

If you don’t feel significantly better after understanding your options and making a plan, something’s wrong with the approach or provider.

4. Questions Aren’t Burdens

Mother of the groom wrote: “Kevin was amazing answered all my dumb questions lol.”

Many people hold back questions, fearing they’re asking too many, taking too much time, or revealing their ignorance. They commit to programs with lingering confusion.

Questions aren’t dumb. They’re critical for informed decision-making. Good specialists welcome questions because unanswered questions lead to misunderstandings that cause dropout. Every question makes success more likely.

Ask every question that occurs to you. If you feel rushed or made to feel stupid for asking, that’s a red flag about the provider. Good specialists encourage questions and treat each one as important.

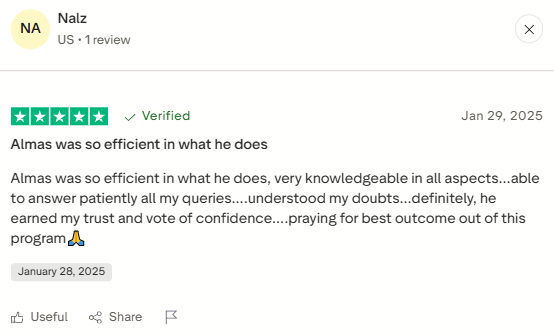

Nalz appreciated: “Almas was so efficient in what he does, very knowledgeable in all aspects…able to answer patiently all my queries….understood my doubts.”

Plan to ask all your questions. Write them down beforehand. If a specialist makes you feel your questions are burdensome, find a different specialist.

Plan to ask all your questions. Write them down beforehand. If a specialist makes you feel your questions are burdensome, find a different specialist.

5. Not Qualifying for Loans Doesn’t Mean No Options

JANET RANK shared: “Maurice was so helpful and kind. I did not qualify for a personal loan and he helped me understand what alleviate could do to help me. And for the first time in a while, I feel very positive about the process.”

Many people think debt consolidation = personal loans. When they don’t qualify for loans, they assume they’re out of options and doomed to struggle alone.

Debt consolidation loans are one option among many. Debt management programs, debt settlement, hybrid approaches—multiple pathways exist. Not qualifying for one doesn’t mean no solutions exist.

If you don’t qualify for consolidation loans, that’s not the end. Companies offering only loans will reject you. Companies offering multiple solutions will find alternatives that fit your situation.

Christopher Browning experienced the contrast: “We called about an offer we got in the mail was not able to get approved for that so he suggested a consolidation plan and we have called several other mail offers and no one else bothered to help us.”

Look for companies offering multiple debt relief pathways, not just loans. If one solution doesn’t fit, alternatives should be available. Single-product companies limit your options unnecessarily.

6. Realistic Timelines Beat Optimistic Fantasies

Paula Siwek emphasized: “he made the terms clear and realistic.”

Many people hope for quick fixes: six months to debt-free, painless solutions, minimal sacrifice required. They commit to programs based on optimistic timelines that aren’t realistic.

Real debt relief takes years, not months. 3-5 years is typical. Programs promising faster results often overpromise and underdeliver. Realistic timelines, while longer, are actually more hopeful because they’re achievable.

When evaluating options, be skeptical of promises that sound too good to be true. Appreciate specialists who set realistic expectations even when timelines are longer. You’re more likely to complete a realistic program than abandon an overpromised one.

Jorge’s clarity exemplifies this: “I can’t wait for these next 3 years to go by and be debt free!”

Debt elimination typically takes 3-7 years, depending on the amount and approach. Accept this timeline. Programs promising much faster results are either unsuitable for your situation or misleading.

Debt elimination typically takes 3-7 years, depending on the amount and approach. Accept this timeline. Programs promising much faster results are either unsuitable for your situation or misleading.

7. The Hardest Part Is Starting, Not Continuing

Tamaira Barnes-Hart expressed: “I can’t even thank you enough for taking care of my debt….I should of done this along time ago. I’m so happy, this made my day!!!!”

Many people delay getting help because they imagine the debt relief process itself will be overwhelming, complicated, and stressful. They put off the call for months or years.

Making the decision and initial call is the hardest part. Once you’re in the process with a clear plan and support, it’s actually easier than continuing to struggle alone. The anticipatory anxiety is worse than the reality.

If fear is keeping you from reaching out, understand that making the call is the most difficult step. The process itself—once you’re in it with good support—is typically more manageable than the endless cycle of minimum payments.

One customer mentioned, “lost a lot of sleep trying to figure things out” before getting help, revealing that the struggle before help is often worse than the structured process after.

The anxiety about getting help is typically worse than actually getting help. If you’re losing sleep, if stress is constant, if you’ve been struggling for months, the call itself is relief, not another burden.

8. Follow-Up Support Matters More Than Initial Setup

Anthony D noted: “I just signed up and so far the process has been great! Chad B. is awesome he’s been answering all my questions quickly. He even followed up which was a nice touch.”

Many people focus entirely on the initial enrollment: rates, terms, and monthly payment. They don’t think about ongoing support needs during the 3-5 year journey.

Debt relief isn’t set-it-and-forget-it. Questions arise. Circumstances change. Continued support throughout the program matters immensely. Companies that disappear after enrollment create problems.

During evaluation, ask about ongoing support:

How do I reach someone with questions?

What happens if my circumstances change?

Who follows up to check my progress?

Companies with strong ongoing support have better completion rates.

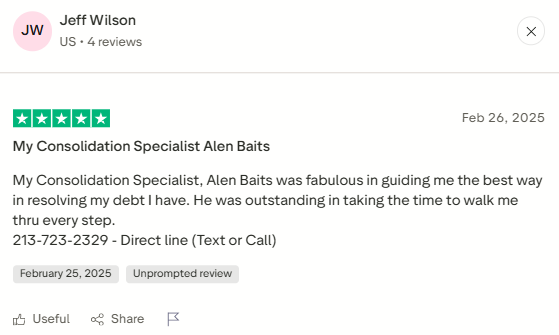

Jeff Wilson valued direct access: “My Consolidation Specialist, Alen Baits was fabulous in guiding me the best way in resolving my debt I have. He was outstanding in taking the time to walk me thru every step.”

Evaluate not just initial setup quality but ongoing support structure. Direct contact with knowledgeable specialists throughout the journey significantly impacts success.

Evaluate not just initial setup quality but ongoing support structure. Direct contact with knowledgeable specialists throughout the journey significantly impacts success.

9. Your Situation Isn’t as Unique as You Think

One customer expressed: “Everyone I spoke with were very understanding, helpful and treated me with such respect. We all encounter some sort of hardship and don’t want to be judged for decisions that were made.”

Many people believe their debt situation is uniquely shameful or complicated. They approach debt relief feeling like their circumstances are unprecedented and indefensible.

Millions of people face debt challenges. Medical emergencies, job loss, divorce, and lack of financial education. Debt consolidation specialists see similar situations constantly.

Don’t let shame about your “unique” situation prevent seeking help. What feels unprecedented to you is familiar to debt relief specialists who’ve seen thousands of cases. Your circumstances aren’t as unusual as you fear.

Grace D experienced understanding: “Kameel was the reason I was even open about this company. Not only did he take the time to help me understand the whole process, he was very kind about it.”

10. Spending Discipline Is Non-Negotiable

David North discovered: “Well, I was a little skeptical at first, but he made a lot of sense in what he was saying as far as me trying to pay two cards off and going with beyond in order to make everything work out very comfortably.”

Many people focus on the debt relief program itself but don’t fully consider the behavioral changes required. They consolidate debt while maintaining spending patterns that created it.

Debt consolidation without spending discipline leads to having both program payments AND new debt. The program solves past debt, but you must prevent new debt accumulation. Behavioral change is essential, not optional.

Before committing to debt consolidation, honestly assess your willingness and ability to change spending habits. If you’re not ready to stop accumulating new debt, consolidation won’t solve your problem. It will just add a new payment on top of continued credit card use.

If you’re not ready for that commitment, work on spending discipline first or choose a program structure that helps enforce it (like debt management plans that close accounts).

11. Patience and Kindness Are Essentials

Katy Shoemaker appreciated: “Chad was really great to work with. He was kind, empathetic, and described the process so clearly. I appreciate having someone like him help me during this time.”

Many people accept poor treatment during debt relief consultations, thinking they should be grateful anyone will help them at all. They tolerate rushedness, condescension, or impersonal service.

Patience and kindness are professional standards that directly impact outcomes. Rushed, impersonal service leads to misunderstanding, inappropriate commitments, and dropout. Quality service is your right, not a gift.

Erick noted: “Luis was a very helpful employee. I never felt talked down to about my financial status and he was very patient throughout the whole process.”

Evaluate how you’re treated during initial contact. If it’s rushed, condescending, or impersonal, expect the same throughout.

12. Accommodations Are Available, You Just Have to Ask

Patricia A Valese appreciated: “This was a great experience because your representative took his time explaining everything to me. He also had much patience since I am hard of hearing.”

Many people with special needs like hearing difficulties, technology challenges, language concerns, and cognitive differences struggle through standard processes without asking for accommodations, thinking none are available.

Accommodations exist for various needs. Good companies adapt to individual circumstances rather than forcing everyone through identical processes. But you often need to communicate your needs for accommodations to be provided.

Mary experienced this compassion: “Alen was my agent and treated me with compassion, respect, and patience. I am compromised with a brain illness that make me vulnerable to financial loss, and Alen’s continual reassurances and non-rushed manner gave me confidence and trust.”

If you have special needs, communicate them upfront. Companies that adapt to individual needs demonstrate commitment to universal accessibility.

13. The Total Cost Matters More Than The Monthly Payment

Many people focus exclusively on the monthly payment amount:

“Can I afford $300/month?”

They don’t calculate total cost: monthly payment × number of months + fees.

A lower monthly payment over a longer term often costs more total than a higher payment over a shorter term.

Always calculate total repayment: monthly payment × months + all fees. Compare this across options. Sometimes the “affordable” option costs thousands more than a slightly higher payment you could manage with budget adjustments.

14. Your Emotional State Will Affect Your Decision

Many people make debt relief decisions while in crisis mode: panicked, desperate, sleep-deprived. They commit to programs without calm, clear thinking.

Emotional state affects decision quality. When possible, take time to reach some emotional stability before committing. If you’re in crisis, acknowledge that and seek extra support to think clearly.

Pressure during panic is predatory; patience during distress is professional.

15. Success Requires Active Participation, Not Passive Hope

Many people think enrolling in a program means “they’ll handle it.” They expect passive participation — just make payments and wait for debt freedom.

Success requires active engagement: sticking to your budget, not accumulating new debt, communicating when circumstances change, and staying motivated through years of payments. The debt relief program provides structure and support, but you provide the discipline and follow-through.

Before enrolling, honestly assess your readiness for active participation. If you’re hoping the program will “fix everything” without your sustained effort, reconsider your readiness or choose programs with more structure and accountability.

You are the primary driver of success. Programs provide a roadmap and support, but you must navigate the journey.

The Bottom Line: Learn Before, Not During

The insights real customers gained through experience are now yours. This knowledge enables:

Better Provider Selection: You know what questions to ask and what quality indicators to look for.

More Informed Decisions: You understand the complete picture, not just marketed highlights.

Appropriate Expectations: You’re prepared for realities, not surprised by them.

Higher Success Probability: You avoid common mistakes that undermine outcomes.

Reduced Stress: You know what’s normal, what to expect, what you deserve.

As hundreds of customers essentially said: “I wish I’d known this before starting.”

Now you do.

Ready to Start With Complete Knowledge?

If you want debt consolidation guidance from specialists who provide the knowledge real customers wish they’d had from day one, LendWyse’s approach is built on these learnings.

Don’t learn these lessons the hard way. Benefit from 600+ customers’ experiences before starting your journey.