Scheduling a debt consultation is a significant step toward regaining financial stability and peace of mind. If you are preparing for your first meeting, you might ask, “What documents do I need for a debt consultation to ensure the session is productive?”

This meeting allows a professional to analyze your financial situation and recommend the best course of action based on your unique circumstances and available debt relief programs.

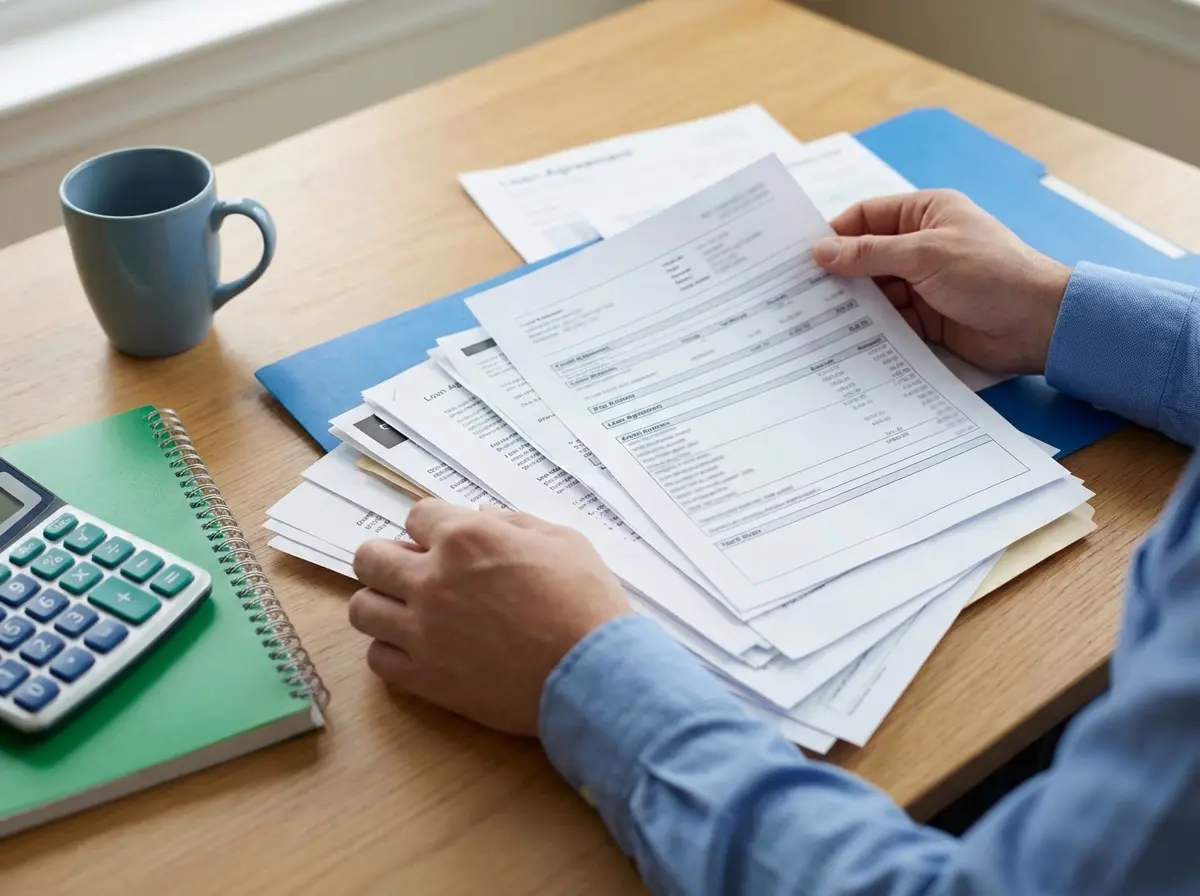

Many people arrive at these appointments with only rough estimates of what they owe or earn. This lack of preparation can lead to vague recommendations that do not actually solve the underlying financial problems. To get a concrete plan, you must bring specific required documentation that paints a clear picture of your finances.

Gathering these papers might seem like a heavy task, but it saves time and prevents follow-up delays. A well-documented file allows the counselor to immediately identify which relief programs you qualify for. The following guide details exactly what you need for a debt consultation to make the most of your appointment.

Personal Identification: What Documents Do I Need for a Debt Consultation?

The first item on your checklist is a valid government-issued identification to confirm who you are. Debt counselors must verify your identity to protect you from fraud and to access your credit report legally. This step establishes the formal relationship between you and the agency assisting you, ensuring that all subsequent financial advice is tailored to your specific legal identity.

You should bring a current driver’s license or a state-issued identification card that is not expired. If you do not have these, a valid passport or military ID will usually suffice for verification purposes. The name on your identification should match the name on your financial accounts to avoid confusion during the verification process.

Most agencies also require your Social Security card or a tax document containing your Social Security number. This number is necessary for pulling your credit report to see a complete history of your obligations. Without it, the counselor cannot see the full scope of your credit profile or your current credit score during the credit counseling session.

Financial Records: Proof of Income and Revenue for Debt Relief Options

Your ability to repay debt or qualify for specific debt relief programs depends entirely on your verifiable income. You must prove exactly how much money flows into your household every month from all sources. This allows the counselor to calculate your debt-to-income ratio, which is a critical metric in professional financial analysis and financial records review.

Employees should provide pay stubs covering the most recent thirty to sixty days of employment. These documents show your gross income, taxes, insurance deductions, and your actual take-home pay. Using your net pay rather than gross pay creates a much more realistic monthly budget for debt repayment.

Self-employed individuals face slightly stricter requirements because their income often fluctuates from month to month. You should bring your two most recent tax returns and profit-and-loss statements for the current year. Bank statements showing deposits can also help substantiate income if your business records are not fully updated.

Do not overlook other sources of revenue that contribute to your monthly household budget. This includes award letters for Social Security, disability benefits, alimony, or child support payments you receive. Even irregular income like quarterly bonuses or commissions should be documented to show your total earning potential.

- Bring a valid government ID and your Social Security number to authorize credit checks.

- Employees need the last 30 to 60 days of pay stubs to verify net income.

- Self-employed individuals must provide tax returns and profit-and-loss statements.

Required Paperwork: Comprehensive Debt Statements for a Debt Management Plan

The core of your credit counseling involves a deep review of exactly who you owe and how much. While a credit report provides an overview, it often lags behind current balances or misses recent fees. You need to supply the most recent billing statements for every single creditor to build an effective debt management plan.

These statements must include credit cards, personal loans, medical bills, and any payday loans. The counselor needs to see the current interest rate (APR), the minimum monthly payment, and the total payoff amount. This specific data helps them calculate how much interest you will pay over time versus debt consolidation loans.

Do not forget to include older debts that may have been sold to debt collection agencies. If you receive letters or calls from collectors, bring those written notices to the meeting. Identifying the current owner of the debt is essential for negotiating settlements or repayment terms.

Never hide a debt from your counselor due to embarrassment. An incomplete list leads to a failed financial plan that will not resolve your issues.

Budgeting Data: Monthly Expense Verification for Your Financial Counselor

Income and debt are only two parts of the equation; knowing where your money goes is equally important. Many people underestimate their spending, so documented proof is better than guessing when working with a financial counselor. You should collect bills that represent your fixed monthly obligations to build an accurate monthly budget and improve the budgeting process.

Start with housing costs, which are typically the largest expense for any household. Bring your mortgage statement, which should show taxes and insurance, or your current lease agreement if you rent. These numbers are non-negotiable “four walls” expenses that must be prioritized above unsecured debt.

Next, gather documentation for utilities like electricity, water, gas, internet, and mobile phone service. Reviewing these bills can sometimes reveal opportunities to cut costs, which frees up cash for debt repayment. Even small reductions in these recurring charges can add up significantly over a year.

Finally, try to estimate variable costs like groceries, fuel, and medical prescriptions using bank statements. Look at the last three months of spending to find a realistic average for these categories. Accurate expense tracking prevents you from agreeing to a monthly debt payment you cannot actually afford.

Asset and Property Documentation for Debt Settlement and Relief

Your assets play a major role in determining which debt relief options, such as debt settlement, are available to you. For example, owning a home with significant equity might open doors to low-interest loans, but it might also complicate bankruptcy filings. You need to provide documents that establish the value of what you own.

If you own real estate, bring a recent appraisal or a current tax assessment to show its value. You should also bring your current mortgage statement to show how much is still owed on the property. The difference between the value and the loan balance is your equity, which is a key financial lever.

Vehicle titles or personal loan statements are also necessary to determine the equity in your cars or trucks. You should also be ready to discuss the value of other significant items like recreational vehicles or boats. In some debt settlement scenarios, liquidating non-essential assets might be suggested to clear balances quickly.

Financial assets like savings accounts, 401(k)s, and IRAs must also be disclosed during the debt consultation. While you should generally avoid draining retirement accounts to pay debt, the counselor needs to know they exist. This helps them give advice that protects your long-term future while solving immediate problems.

- Bring recent statements for all credit cards, loans, and collection notices.

- Document fixed expenses like rent and utilities to create a realistic budget.

- Provide records of assets like homes and cars to determine your net worth.

Legal Records: Court and Legal Notices for Debt Consolidation

If your financial situation has progressed to legal action, you must bring all related paperwork to discuss potential debt consolidation or relief. This includes any court summons, judgments, or wage garnishment notices you have received. These documents change the urgency of your situation and limit the strategies a counselor can recommend.

A judgment against you gives a creditor the right to take aggressive collection actions. If you have received a notice of a lawsuit, the timeline to respond is usually very short. Showing these papers to your consultant immediately allows them to prioritize these critical threats over other debts.

You should also include documentation regarding any previous bankruptcy filings or divorce decrees. A divorce decree often outlines who is responsible for specific joint debts, which impacts your liability. Previous bankruptcies affect your eligibility for filing again, so the counselor needs the dates and discharge details.

Credit Counseling Preparation: How to Organize Your Financial File

Bringing a shoebox full of crumpled receipts is not the most efficient way to handle your consultation. Organizing your documents beforehand shows you are serious and helps the meeting run smoothly. Follow these steps to prepare a file that makes the process easier for everyone involved.

How to Prepare Your Documents

Categorize Your Paperwork

Separate your documents into four distinct piles: Income, Debts, Expenses, and Assets. Use paperclips or folders to keep each category distinct and tidy.

Highlight Critical Numbers

Go through your statements and use a highlighter to mark the total balance, interest rate, and minimum payment. This draws the eye to the data that matters most.

Create a Summary Sheet

Write a simple one-page summary listing your total monthly income and total estimated debt. This provides a quick snapshot before digging into the details.

Final Thoughts on Preparation

Arriving at your debt consultation with the right documents transforms the experience from a stressful conversation into a strategic planning session. When you present clear proof of your income, expenses, and debts, the counselor can build a plan that actually works for your life. You avoid the frustration of having to call back later with missing information.

Remember that this meeting is confidential and designed to help you, not judge you. The more transparent you are with your documentation, the faster you can find a path out of debt. Take the time to gather these papers today, and you will be ready to take control of your financial future.

Debt won’t fix itself — but the right plan can. Use Simple Debt Solutions to compare multiple loan offers in one place and find the option that helps you pay less and get out of debt faster.